Mortgage Closing Costs are fees that are paid to the mortgage lender and its partners to complete the home-buying transaction. Prospective home buyers need to pay for the closing costs as well as the down payments, which is a percentage of the home price paid upfront as part of the home loan.

The Mortgage Closing costs and fees may include buying down the rate, title insurance, appraisals, upfront property taxes, loan origination fees, and much more. These fees vary depending on the mortgage lenders and the situation, so make sure the borrowers review them upfront so they can get an idea of the total costs.

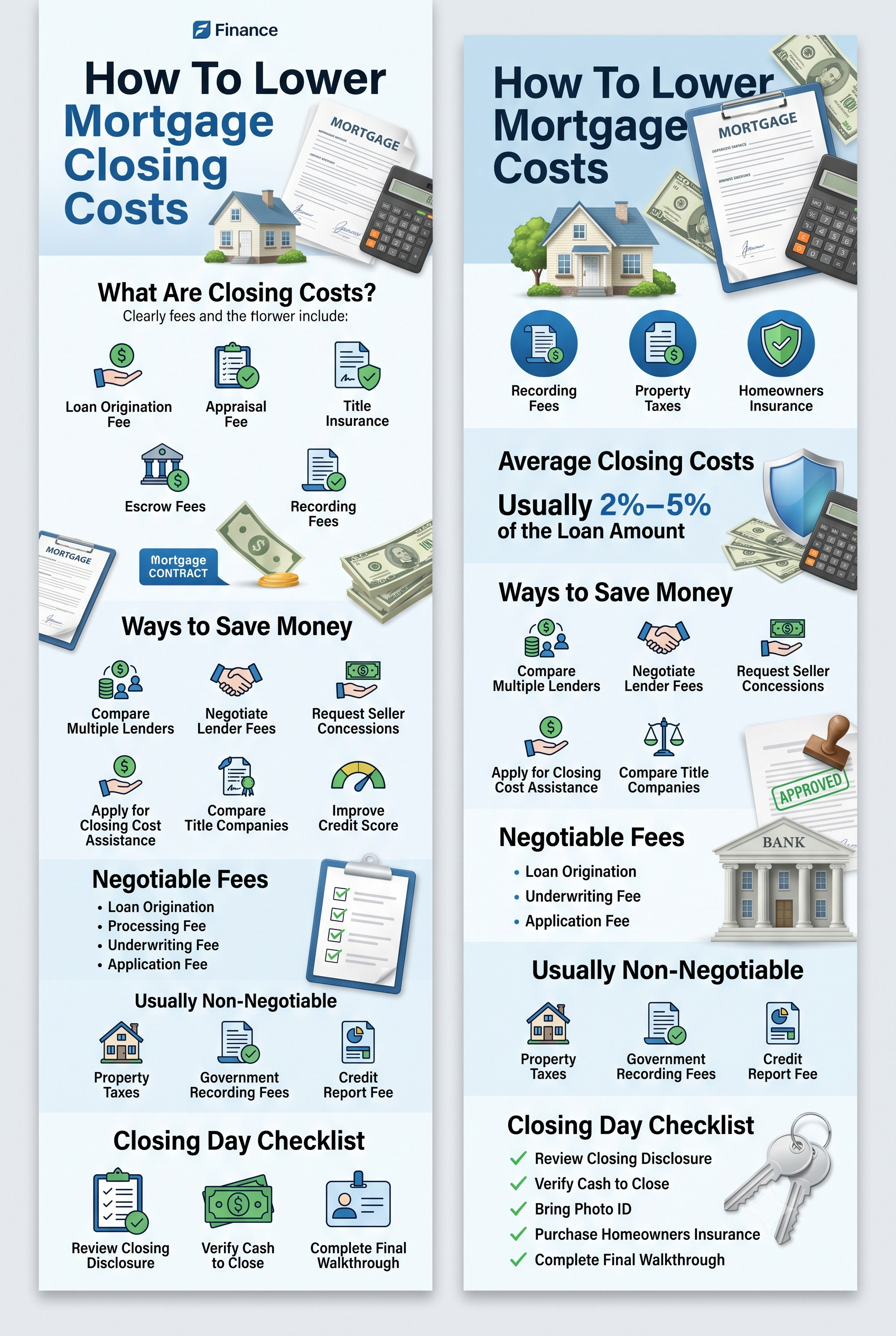

The Mortgage closing costs typically equal 1 percent to 5 percent of the home’s purchase price which are the extra fees due at closing for various services related to purchasing a property.

Buying a home is exciting until you reach the point where someone hands you a long list of fees you’ve probably never heard of. Suddenly, you’re looking at loan origination fees, title insurance, appraisal charges, escrow fees, prepaid expenses, and dozens of other costs that weren’t part of the home’s advertised price. That’s where many buyers feel overwhelmed.

The good news? You don’t have to accept every fee without question.

Learning how to lower mortgage closing costs can easily save you hundreds—or even thousands—of dollars before you receive the keys to your new home. Many buyers assume every closing expense is fixed, but that’s simply not true. Several lender fees are negotiable, some third-party services can be shopped around, and numerous state and federal assistance programs help qualified buyers reduce upfront expenses.

According to recent mortgage industry data, most U.S. buyers pay between 2% and 5% of the loan amount in closing costs, although the exact amount depends on the property, lender, loan type, and location. Loan Estimates and Closing Disclosures are specifically designed to help buyers compare offers before signing.

Whether you’re purchasing your first home, refinancing, or simply trying to understand your mortgage paperwork, this guide explains every major fee in plain English while showing practical ways to reduce your total mortgage closing costs legally.

What Are Mortgage Closing Costs?

If you’ve ever wondered why buying a home costs much more than the purchase price, closing costs are the answer.

Closing costs are the collection of fees paid to complete a real estate transaction. They cover everything required to verify the property’s legal ownership, process your mortgage, evaluate your credit, protect the lender, and officially transfer ownership.

Think of buying a house like buying a car—but on a much larger scale. Before you drive away, numerous professionals have already done work behind the scenes. Appraisers determine the property’s value. Title companies verify ownership history. Underwriters review your financial information. Local governments record the transaction. Insurance providers prepare coverage. Each professional charges a fee.

These expenses are typically paid on closing day and are separate from your down payment.

Most buyers pay costs such as:

- Loan origination fee

- Appraisal fee

- Credit report fee

- Title insurance

- Title search fees

- Escrow fees

- Recording fees

- Underwriting fee

- Processing fee

- Prepaid property taxes

- Homeowners insurance premiums

- Mortgage insurance (when applicable)

Although many people think these charges are fixed, several can be negotiated or reduced through comparison shopping, lender competition, or seller concessions. That’s why understanding every fee before signing is one of the smartest financial decisions a homebuyer can make.

How Much Are Closing Costs in the United States?

One of the first questions buyers ask is:

“How much are closing costs?”

There’s no universal answer because every mortgage is different.

Most lenders estimate average closing costs at around 2% to 5% of the total mortgage amount. For example:

| Home Loan | Estimated Closing Costs (2%–5%) |

|---|---|

| $200,000 | $4,000–$10,000 |

| $300,000 | $6,000–$15,000 |

| $400,000 | $8,000–$20,000 |

| $500,000 | $10,000–$25,000 |

Recent industry reports also estimate that the average borrower paid approximately $4,661 in closing costs for a single-family home purchase, excluding real estate commissions, though costs vary significantly by state and loan type.

Several factors influence your final costs:

- Home purchase price

- Loan amount

- Credit profile

- State taxes

- Local recording fees

- Mortgage lender fees

- Whether you’re paying discount points

- Escrow requirements

- Property tax rates

- Homeowners insurance costs

Using a closing costs calculator early in your home search helps you estimate how much cash you’ll actually need beyond your down payment. Comparing Loan Estimates from multiple lenders is another highly effective strategy because different lenders often charge different origination, underwriting, and processing fees.

Complete Breakdown of Typical Mortgage Closing Costs

Understanding each fee makes it much easier to identify opportunities to save money.

| Fee | Purpose | Usually Negotiable? |

|---|---|---|

| Loan Origination Fee | Lender processing | Yes |

| Underwriting Fee | Loan approval review | Often |

| Processing Fee | Administrative work | Often |

| Appraisal Fee | Determines property value | Limited |

| Credit Report Fee | Credit check | Usually No |

| Title Search Fees | Ownership verification | Yes (provider) |

| Title Insurance | Protects buyer/lender | Yes (shop around) |

| Escrow Fees | Handles transaction funds | Sometimes |

| Recording Fees | Government filing | No |

| Property Taxes | Prepaid taxes | No |

| Homeowners Insurance | Insurance premium | Yes (shop providers) |

| Mortgage Insurance | Required for some loans | Limited |

The key takeaway is simple:

Some fees are determined by government agencies or outside vendors, while others are controlled directly by your lender. Those lender-controlled charges are where buyers often find the biggest opportunities to reduce costs.

Negotiable vs. Non-Negotiable Closing Costs

One of the biggest misconceptions among homebuyers is that every fee listed on the Loan Estimate is set in stone. That simply isn’t true. While some costs are required by law or determined by third parties, many lender-imposed charges can be discussed, reduced, or even eliminated if you know what to ask.

Think of your mortgage like shopping for a new vehicle. Two dealerships may sell the same model, but one offers lower documentation fees, a better financing package, or additional incentives. Mortgage lenders operate in much the same way. Interest rates may look similar, but the fees attached to the loan can vary by hundreds or even thousands of dollars.

Here’s a quick comparison:

| Closing Cost | Usually Negotiable? | Tips |

|---|---|---|

| Loan Origination Fee | ✅ Yes | Ask for a reduction or waiver. |

| Underwriting Fee | ✅ Often | Compare with competing lenders. |

| Processing Fee | ✅ Often | Request a discount. |

| Application Fee | ✅ Sometimes | Some lenders remove it to earn your business. |

| Rate Lock Fee | ✅ Sometimes | Ask if promotional waivers are available. |

| Appraisal Fee | ❌ Rarely | Typically paid to an independent appraiser. |

| Credit Report Fee | ❌ No | Fixed third-party cost. |

| Recording Fees | ❌ No | Set by local government. |

| Property Taxes | ❌ No | Government requirement. |

| Homeowners Insurance | ✅ Yes | Shop around for better rates. |

| Title Insurance | ✅ Yes | Compare title companies where allowed by state law. |

| Escrow Fees | ✅ Sometimes | Compare settlement providers if permitted. |

Knowing which fees are negotiable helps you focus your efforts where they’ll have the biggest financial impact instead of wasting time trying to negotiate costs that are fixed.

How to Compare Mortgage Lenders and Save Thousands?

Many buyers spend weeks comparing home prices but only a few minutes comparing lenders. That can be an expensive mistake.

Every mortgage lender has its own pricing structure. One lender may advertise a slightly lower interest rate but charge significantly higher lender fees. Another may offer a competitive rate with reduced closing costs or lender credits. Looking only at the interest rate doesn’t tell the full story.

The smartest approach is to request Loan Estimates from at least three different lenders within a short time frame. Credit scoring models generally treat multiple mortgage inquiries made within a designated shopping window as a single inquiry, allowing you to compare offers without significantly affecting your credit score.

When reviewing Loan Estimates, compare:

- Interest rate

- Annual Percentage Rate (APR)

- Loan origination fee

- Underwriting fee

- Processing fee

- Discount points

- Lender credits

- Estimated cash to close

Sometimes a lender offering a slightly higher interest rate may save you more upfront by reducing or eliminating several closing costs. This can be especially helpful if you don’t plan to stay in the home for many years.

Expert Tip

Create a simple spreadsheet listing each lender’s fees side by side. The differences become much easier to spot, and you’ll have concrete numbers to use when negotiating.

How to Negotiate Closing Costs with Your Lender?

Many homebuyers never ask for discounts because they assume the lender’s first offer is final. In reality, lenders often have flexibility, especially in competitive markets.

Negotiation doesn’t have to be confrontational. A polite, informed conversation backed by competing Loan Estimates can go a long way. If another lender offers lower origination or processing fees, let your preferred lender know. They may match the offer or provide additional lender credits to keep your business.

Here are practical negotiation strategies:

- Ask whether the loan origination fee can be reduced.

- Request that administrative fees be waived.

- Compare lender fees with competing quotes.

- Inquire about promotional offers for first-time buyers.

- Ask if lender credits are available in exchange for a slightly higher interest rate.

- Question duplicate or unclear charges on the Loan Estimate.

- Request an explanation for every fee you don’t understand.

Remember, asking questions is part of the process. A reputable lender should be willing to explain each charge clearly and justify why it’s included.

Warning: Never sign your final paperwork if you notice unexpected fees that weren’t disclosed earlier. Compare your Closing Disclosure carefully against your original Loan Estimate and ask about any significant differences.

Understanding Loan Estimates vs. Closing Disclosure

Two of the most important documents you’ll receive during the mortgage process are the Loan Estimate and the Closing Disclosure. Understanding how they work can prevent costly surprises.

The Loan Estimate is provided shortly after you apply for a mortgage. It outlines the projected interest rate, monthly payment, loan terms, and estimated closing costs. Think of it as a preview of what your mortgage will likely cost.

The Closing Disclosure arrives at least three business days before closing. It contains the final numbers you’ll actually pay on closing day.

Here’s a simple comparison:

| Feature | Loan Estimate | Closing Disclosure |

|---|---|---|

| Issued | Shortly after application | At least 3 business days before closing |

| Purpose | Estimated costs | Final confirmed costs |

| Interest Rate | Estimated or locked | Final |

| Closing Costs | Estimated | Final |

| Cash to Close | Estimated | Final amount |

When reviewing the Closing Disclosure:

- Compare every fee with your Loan Estimate.

- Look for unexpected increases.

- Verify the loan amount and interest rate.

- Confirm your prepaid taxes and insurance.

- Double-check the total cash needed at closing.

If something looks different, ask your lender for an explanation before signing. Even small discrepancies can add hundreds of dollars to your closing costs.

Seller Concessions: Let the Seller Help Cover Closing Costs

One of the most effective ways to lower your out-of-pocket expenses is through seller concessions. Instead of reducing the home’s purchase price, the seller agrees to pay part of the buyer’s closing costs.

Seller concessions are especially common in markets where buyers have stronger negotiating power. Rather than lowering the sale price, sellers may find it easier to contribute toward closing costs to keep the transaction moving.

For example, imagine you’re buying a home for $350,000, and your closing costs total $9,000. If the seller agrees to contribute $6,000, your required cash at closing drops significantly. That can make a big difference if you’re trying to preserve savings for moving expenses, furniture, or emergency funds.

Keep in mind that the maximum seller contribution depends on the type of mortgage and your down payment. FHA, VA, USDA, and conventional loans each have different limits on seller concessions.

Seller concessions won’t always be available, particularly in highly competitive housing markets, but they’re well worth discussing with your real estate agent during negotiations.

Understanding Lender Credits: A Smart Way to Reduce Upfront Costs

If you’re looking for ways to lower your mortgage closing costs without delaying your home purchase, lender credits deserve serious consideration.

A lender credit is exactly what it sounds like—the lender agrees to pay some or all of your closing costs. In exchange, you’ll usually accept a slightly higher mortgage interest rate. While this means your monthly payment may be a little higher, it can significantly reduce the amount of cash you need on closing day.

For many buyers, especially first-time homebuyers, coming up with thousands of dollars in upfront costs is more difficult than paying a few extra dollars each month. That’s where lender credits can be a practical solution.

Example

Suppose your closing costs total $8,000.

You have two loan options:

| Option | Interest Rate | Closing Costs |

|---|---|---|

| Standard Loan | 6.25% | $8,000 |

| Loan with Lender Credits | 6.50% | $3,000 |

If you plan to sell or refinance within a few years, paying a slightly higher interest rate may actually save you money overall because you’ll avoid paying thousands upfront.

However, if you’re planning to stay in the home for 20 or 30 years, carefully calculate whether the higher monthly payment outweighs the upfront savings. Your lender can help you compare the long-term costs of each option.

Should You Buy Discount Points?

Many buyers are confused by discount points, sometimes called mortgage points. They sound complicated, but the concept is fairly straightforward.

A discount point is a fee you pay at closing to reduce your mortgage interest rate. In most cases, one point costs 1% of your loan amount.

For example:

- Loan Amount: $400,000

- One Discount Point: $4,000

Paying that $4,000 upfront may reduce your interest rate enough to lower your monthly payment for the life of the loan.

The key question is: Will you stay in the home long enough to recover the cost?

If you expect to own the property for many years, buying points can lead to substantial savings over time. But if you anticipate moving or refinancing within a few years, you may never reach the break-even point.

A Simple Rule of Thumb

Consider buying discount points if:

- You have extra cash available.

- You plan to stay in the home for at least seven to ten years.

- The monthly savings exceed the upfront cost over time.

Skip discount points if:

- Cash is tight.

- You’re buying your first home and need liquidity.

- You expect to refinance soon.

- You’re unsure how long you’ll keep the property.

Always ask your lender to calculate the break-even period before deciding.

Closing Cost Assistance Programs for First-Time Home Buyers

One of the biggest surprises for many buyers is discovering that they may qualify for financial assistance they didn’t even know existed.

Across the United States, thousands of closing cost assistance programs help eligible buyers cover expenses such as:

- Loan origination fees

- Title costs

- Appraisal fees

- Down payment assistance

- Closing costs

- Mortgage insurance

- Other eligible home-buying expenses

These programs are offered through state housing finance agencies, local governments, nonprofit organizations, and occasionally employers.

Eligibility often depends on factors such as:

- Household income

- Credit score

- Home purchase price

- Property location

- First-time homebuyer status

Some programs provide grants that never need to be repaid. Others offer forgivable loans that disappear after you’ve lived in the home for a certain number of years.

If you’re purchasing your first home, ask your lender and real estate agent about available assistance before signing a purchase agreement. A little research could save you several thousand dollars.

FHA vs. VA vs. Conventional Loan Closing Costs

Not every mortgage program has the same closing costs. Understanding the differences can help you choose the option that best fits your financial situation.

| Loan Type | Typical Closing Costs | Special Notes |

|---|---|---|

| Conventional Loan | Moderate | Flexible lender options and negotiable fees. |

| FHA Loan | Moderate | Includes upfront mortgage insurance premium unless financed. |

| VA Loan | Often Lower | Many borrowers avoid mortgage insurance, but a VA funding fee may apply. |

| USDA Loan | Moderate | May include guarantee fees but offers benefits for eligible rural buyers. |

Conventional Loans

These loans generally provide the most flexibility. You can shop among many lenders, compare fees, and negotiate several charges.

FHA Loans

FHA loans are popular with first-time buyers because of their lower down payment requirements. However, borrowers should account for the upfront mortgage insurance premium and ongoing mortgage insurance payments.

VA Loans

Eligible veterans, active-duty service members, and certain surviving spouses often benefit from lower closing costs. VA loans typically don’t require monthly mortgage insurance, although many borrowers pay a one-time VA funding fee.

Choosing the right loan involves much more than comparing interest rates. Always evaluate the complete picture, including closing costs, monthly payments, mortgage insurance, and long-term affordability.

Hidden Mortgage Fees to Watch Out For

Most closing costs are legitimate, but buyers should still review every line of their paperwork carefully. Occasionally, you’ll encounter fees that deserve a second look.

Some examples include:

- Excessive processing fees

- Duplicate administrative charges

- Courier or overnight delivery fees

- Unnecessary document preparation fees

- High rate-lock extension charges

- Inflated settlement service costs

Not every extra fee is inappropriate, but you should understand exactly why you’re paying it.

Questions to Ask Your Lender

- What does this fee cover?

- Is this required?

- Can this charge be reduced or waived?

- Is there a less expensive service provider available?

- Why is this fee higher than another lender’s quote?

If the explanation isn’t clear, don’t hesitate to ask again. You’re making one of the largest financial decisions of your life, and you have every right to understand every dollar you’re paying.

Prepaid Expenses Aren’t Really Closing Costs

Many buyers are surprised when they discover that a significant portion of their “closing costs” isn’t actually made up of fees at all.

Instead, they’re prepaid expenses, which are funds collected in advance to ensure certain bills are paid after you become the homeowner.

Common prepaid expenses include:

- Property taxes

- Homeowners insurance premiums

- Mortgage interest from the closing date until the first payment

- Initial escrow deposits

These aren’t charges that enrich your lender. Instead, they’re payments you’ll owe anyway as a homeowner—they’re simply collected upfront.

Understanding this distinction helps buyers better prepare their budget and avoid confusion when reviewing the Closing Disclosure.

Reviewing Your Closing Disclosure Before Signing

The Closing Disclosure is one of the most important documents you’ll receive during the home-buying process. By law, your lender must provide it at least three business days before closing, giving you time to review the final loan terms and costs.

Don’t treat this document as just another stack of paperwork. It’s your last opportunity to verify that everything matches what you agreed to earlier. Even small errors can cost you hundreds or thousands of dollars.

When reviewing your Closing Disclosure, pay close attention to:

- Loan amount – Make sure it matches your approved mortgage.

- Interest rate – Verify it matches your locked rate.

- Monthly payment – Confirm the amount aligns with your expectations.

- Cash to close – Double-check the total amount you’ll need on closing day.

- Closing costs – Compare every fee against your original Loan Estimate.

- Prepaid expenses – Ensure taxes, insurance, and escrow deposits are accurate.

Watch for These Red Flags

- Unexpected lender fees

- Charges that weren’t on your Loan Estimate

- Duplicate fees

- Incorrect property taxes

- Wrong homeowners insurance premium

- Errors in your name, address, or loan terms

If you notice anything that doesn’t make sense, don’t be afraid to ask questions. A legitimate lender will gladly explain every charge. Never feel pressured to sign documents you don’t fully understand.

Mortgage Refinancing Closing Costs

Many homeowners refinance to lower their interest rate, reduce monthly payments, or change their loan term. While refinancing can save money over time, it’s important to remember that refinancing closing costs still apply.

Typical refinance costs include:

- Loan origination fee

- Appraisal fee (if required)

- Credit report fee

- Title search

- Title insurance (varies by state)

- Recording fees

- Underwriting fee

- Processing fee

Refinance closing costs generally range from 2% to 5% of the loan amount, similar to a purchase mortgage.

Is Refinancing Worth It?

Ask yourself:

- How much will my monthly payment decrease?

- How long will it take to recover the closing costs?

- Do I plan to stay in the home beyond the break-even point?

For example, if refinancing costs $5,000 but saves $200 per month, you’ll recover your investment in about 25 months. If you plan to stay much longer than that, refinancing could be a smart financial move.

Mortgage Closing Checklist

Before heading to the closing table, use this checklist to help ensure everything is in order.

Before Closing Day

- ✔ Compare Loan Estimate and Closing Disclosure

- ✔ Review every lender’s fee

- ✔ Confirm your interest rate

- ✔ Verify the cash-to-close amount

- ✔ Arrange a wire transfer or certified funds

- ✔ Purchase homeowners insurance

- ✔ Review the title report

- ✔ Schedule a final walkthrough of the property

- ✔ Bring a government-issued photo ID

- ✔ Ask questions about anything you don’t understand

Having a checklist helps reduce stress and minimizes the chance of last-minute surprises.

Expert Money-Saving Tips to Lower Mortgage Closing Costs

If your goal is to save as much money as possible, combine several of these strategies instead of relying on just one.

1. Shop Multiple Lenders

Always compare at least three lenders. Even if the interest rates are similar, lender fees often vary significantly.

2. Negotiate Fees

Ask whether application, processing, underwriting, or origination fees can be reduced or waived.

3. Request Seller Concessions

In the right market, sellers may agree to pay part of your closing costs instead of lowering the home’s purchase price.

4. Compare Title Companies

In many states, buyers are free to choose their own title company. Shopping around can lead to meaningful savings.

5. Consider Lender Credits

If upfront cash is limited, lender credits can reduce your closing costs in exchange for a slightly higher interest rate.

6. Apply for Assistance Programs

State and local programs may provide grants or forgivable loans for qualified buyers.

7. Review Every Fee

Never assume every charge is correct. Ask your lender to explain anything you don’t recognize.

8. Improve Your Credit Before Applying

A stronger credit score may qualify you for better loan pricing and lower lender fees.

9. Lock Your Interest Rate Wisely

Rate fluctuations can affect both your monthly payment and overall loan costs. Discuss timing with your lender.

10. Budget Early

Use a closing costs calculator and build these expenses into your savings plan long before closing day.

Conclusion

Learning how to lower mortgage closing costs is one of the smartest financial moves any homebuyer can make. While some expenses—such as government recording fees and property taxes—are generally fixed, many lender fees are negotiable, and there are numerous opportunities to reduce your upfront costs through comparison shopping, seller concessions, lender credits, and assistance programs.

The key is preparation. Review your Loan Estimate, compare offers from multiple lenders, understand every fee listed on your Closing Disclosure, and don’t hesitate to ask questions. A few hours of research and negotiation can translate into thousands of dollars in savings.

Buying a home is a major milestone, but it doesn’t have to drain your savings. By understanding the closing process and making informed decisions, you’ll be in a stronger financial position from day one of homeownership.

Frequently Asked Questions (FAQs)

1. What are closing costs?

Closing costs are the fees and prepaid expenses required to complete a real estate transaction. They typically include lender fees, title services, appraisal costs, escrow charges, recording fees, prepaid property taxes, and homeowners insurance.

2. Who pays closing costs?

Both buyers and sellers usually pay closing costs, but the exact responsibilities depend on local customs, the purchase agreement, and the type of mortgage. Buyers generally pay lender-related fees, while sellers often cover agent commissions and certain transfer costs.

3. Are closing costs negotiable?

Yes. Many lender-controlled fees—such as loan origination, processing, and underwriting fees—can often be negotiated. Third-party costs and government fees are generally less flexible.

4. Can sellers pay my closing costs?

Yes. Through seller concessions, sellers may agree to contribute toward some or all of the buyer’s closing costs, subject to loan program limits.

5. Can I roll closing costs into my mortgage?

In some refinance transactions, borrowers may be able to roll closing costs into the new loan balance. For home purchases, this option is more limited and depends on the loan program and lender guidelines.