Can You Get a Mortgage With Student Loan Debt: Buying your first home is exciting, but it can also feel overwhelming when you have student loan debt hanging over your finances. Many first-time home buyers assume that carrying student loans automatically disqualifies them from getting a mortgage. Thankfully, that’s one of the biggest misconceptions in the home-buying world.

The reality is much more encouraging. Millions of Americans successfully purchase homes every year while still repaying student loans. Mortgage lenders rarely reject applicants simply because they have education debt. Instead, they carefully examine how that debt fits into the bigger picture of your financial health. Your income, credit score, debt-to-income ratio, employment history, savings, and down payment all play significant roles in determining whether you qualify.

Another common concern is whether federal repayment programs, deferred loans, or student loan forgiveness affect mortgage eligibility. These factors do matter, but not always in the way borrowers expect. Different loan programs—including Conventional, FHA, VA, and USDA mortgages—may calculate student loan obligations differently, and lender requirements can vary. That’s why understanding the rules before you apply can dramatically improve your chances of approval.

This guide explains everything you need to know about getting a mortgage while paying student loans. You’ll learn how lenders calculate debt, which mortgage options are the most flexible, practical ways to improve your approval odds, and mistakes that could delay your home purchase. While mortgage guidelines evolve over time, the strategies covered here remain valuable for most borrowers. Always verify current requirements with your chosen mortgage lender before applying.

What Is Student Loan Debt?

Student loan debt is money borrowed to pay for higher education that must usually be repaid with interest. Mortgage lenders consider these monthly payments when evaluating your debt-to-income ratio, but having student loans alone does not prevent you from qualifying for a mortgage.

Student loans generally fall into two broad categories: federal and private. Federal student loans are issued or backed by the U.S. government and often provide flexible repayment options, including income-driven repayment plans and temporary payment relief during qualifying circumstances. Private student loans are offered by banks, credit unions, and other financial institutions. Their repayment terms vary widely depending on the lender.

Understanding the type of student loan you have matters because mortgage lenders may evaluate repayment obligations differently. For example, borrowers enrolled in an income-driven repayment plan often have lower required monthly payments than borrowers on standard repayment plans. Those lower payments may positively affect debt-to-income calculations, depending on lender guidelines.

Many borrowers worry about the total amount they owe. Surprisingly, mortgage lenders usually focus less on the total balance and more on the required monthly payment. Someone owing $150,000 with a manageable monthly payment and high income could qualify more easily than someone owing $30,000 but struggling with limited income. This highlights why overall financial stability matters far more than one debt figure alone.

Federal vs. Private Student Loans

Federal student loans generally offer:

- Income-driven repayment options

- Temporary hardship assistance

- Forgiveness programs for qualifying borrowers

- Flexible repayment terms

Private student loans often provide:

- Fixed or variable interest rates

- Fewer repayment protections

- Lender-specific policies

- Limited hardship programs

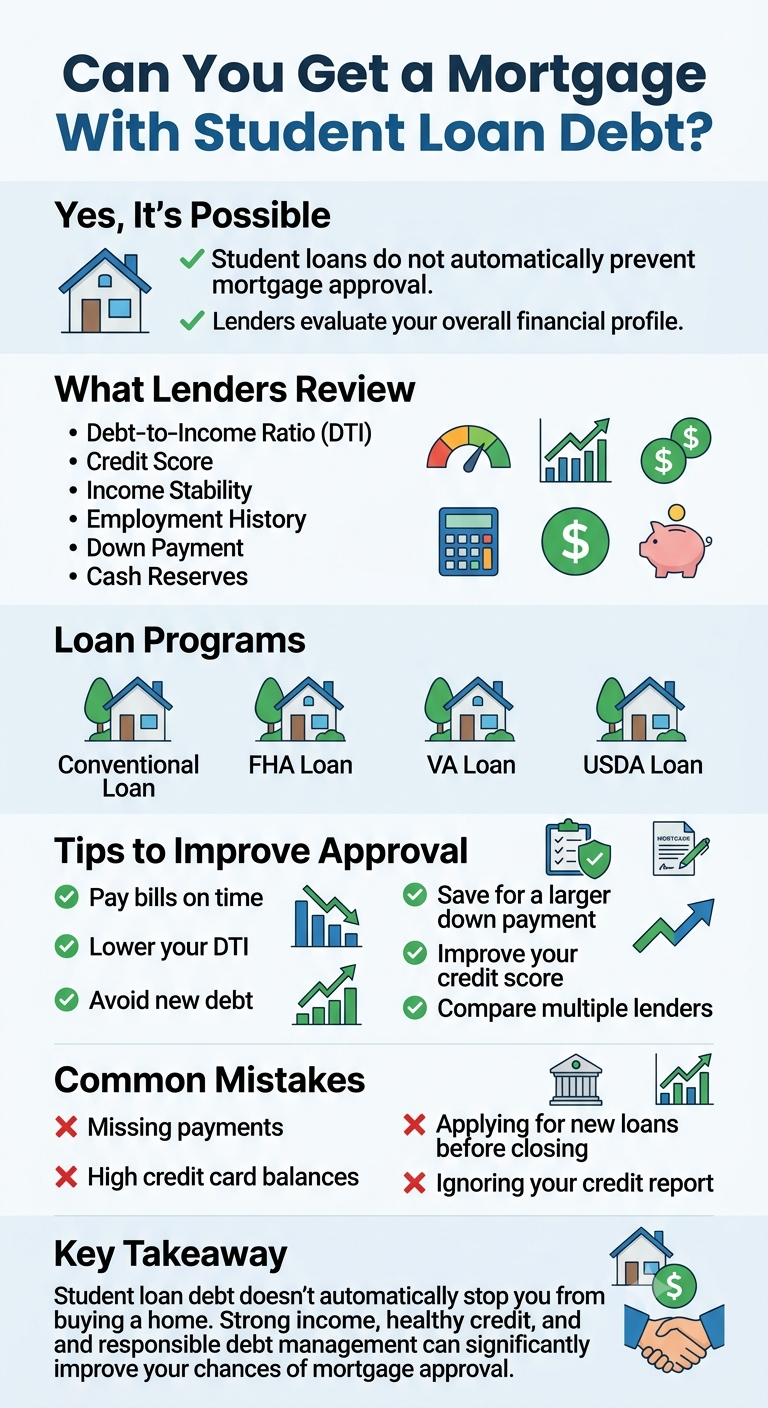

Can Student Loans Affect Mortgage Approval?

Yes. Student loans can affect mortgage approval because lenders include monthly student loan payments when calculating your debt-to-income ratio. However, student loans alone rarely cause a mortgage denial if your income, credit score, savings, and overall financial profile meet the lender’s requirements.

Many first-time home buyers assume their student debt immediately puts homeownership out of reach. Fortunately, mortgage underwriting is much more balanced than that. Lenders evaluate your entire financial picture rather than making decisions based on one type of debt. Student loans are simply one factor among many.

Your debt-to-income ratio, commonly called DTI, measures how much of your monthly income goes toward debt payments. Mortgage lenders use this ratio because it helps predict whether you’ll comfortably afford future mortgage payments. If student loan payments consume a large percentage of your monthly income, qualifying may become more difficult. On the other hand, borrowers with steady employment, healthy savings, and strong credit often qualify even with significant student loan balances.

Credit history also plays an important role. Making student loan payments consistently demonstrates responsible borrowing behavior, which may strengthen your mortgage application. Late payments, defaults, or loan delinquencies can negatively affect both your credit score and lender confidence.

Most lenders also evaluate additional factors, including:

- Employment stability

- Cash reserves

- Down payment amount

- Credit utilization

- Payment history

- Existing monthly obligations

A common misconception is that paying off every student loan before buying a home is always the smartest strategy. Depending on your financial profile, saving for a larger down payment or improving your emergency fund may provide greater benefits than aggressively eliminating low-interest student debt.

How Mortgage Lenders Calculate Student Loan Payments?

Mortgage lenders don’t simply look at your loan balance—they focus on your required monthly obligation. The calculation method depends on the type of mortgage you’re applying for and current underwriting guidelines.

For borrowers making regular monthly payments, lenders generally use the documented payment shown on the credit report or loan statements. Borrowers using income-driven repayment plans may benefit because their required payments often reflect actual income rather than the original loan amount. In many cases, this can lower the calculated debt-to-income ratio and improve mortgage eligibility.

Deferred student loans create another situation. Some borrowers mistakenly believe deferred loans are ignored during mortgage approval. In reality, lenders usually must account for future repayment in some way, even if payments are temporarily paused. The exact calculation varies depending on loan program requirements and lender overlays.

Because mortgage guidelines periodically change, it’s wise to ask your lender exactly how they calculate student loan obligations before applying. Small differences in underwriting can meaningfully affect how much home you qualify for.

What Debt-to-Income Ratio Do Mortgage Lenders Prefer?

Most mortgage lenders prefer a debt-to-income (DTI) ratio below 36%, although many loan programs allow higher ratios if borrowers have strong credit, stable income, cash reserves, or other compensating factors. The acceptable DTI ultimately depends on the mortgage program and the lender’s underwriting guidelines.

Your debt-to-income ratio is one of the most important numbers in the mortgage approval process. It compares your total monthly debt payments—including student loans, auto loans, credit cards, and the proposed mortgage payment—to your gross monthly income before taxes. Think of it as a financial health check. Instead of asking how much you owe in total, lenders want to know whether your monthly income comfortably supports your existing obligations and your future mortgage payment.

Many first-time home buyers worry after calculating their DTI because they assume any ratio above 36% means automatic rejection. That’s rarely the case. Conventional loans often favor lower DTIs, but borrowers with excellent credit scores, larger down payments, or substantial savings may still qualify with higher ratios. Government-backed loan programs such as FHA loans can also offer more flexibility for qualified applicants. Since lenders evaluate the complete financial picture, improving one area—such as your credit score or savings—can sometimes offset a slightly higher DTI.

Front-End vs. Back-End DTI

Mortgage lenders generally evaluate two different DTI calculations:

| Type | What It Includes | Why It Matters |

|---|---|---|

| Front-End DTI | Proposed housing expenses only | Measures housing affordability |

| Back-End DTI | Housing costs plus all monthly debts | Primary ratio used for mortgage approval |

The back-end DTI usually receives the most attention because it reflects your overall monthly financial commitments. If your student loan payment is relatively small compared to your income, it may have only a modest impact on your mortgage eligibility. On the other hand, combining large student loan payments with significant credit card balances and auto loans could push your DTI beyond the lender’s preferred range.

One practical strategy is to calculate your DTI before applying for a mortgage. Doing so allows you to identify potential issues early and gives you time to reduce debt, increase income, or delay a home purchase until your financial profile becomes stronger.

Can You Buy a House While Paying Student Loans?

Yes. Many borrowers successfully buy homes while repaying student loans. Mortgage approval depends on your overall financial profile—including income, credit score, debt-to-income ratio, employment history, and savings—not simply on whether you have student loan debt.

The answer surprises many prospective buyers because student loans have become incredibly common. Millions of Americans carry education debt while purchasing homes, starting families, and building wealth. Mortgage lenders understand this reality. They know that responsible borrowers can manage student loans and homeownership simultaneously.

Buying a home while repaying student loans often comes down to careful financial planning rather than eliminating every dollar of education debt first. Suppose two buyers each earn $90,000 annually. One owes $80,000 in student loans with a manageable monthly payment under an income-driven repayment plan. The other has no student loans but carries significant credit card debt with high interest rates. In many cases, the first borrower may actually present the stronger mortgage application because their overall financial profile appears healthier.

Saving for a down payment remains equally important. Even if you qualify with student debt, maintaining emergency savings after closing helps reduce financial stress during homeownership. Unexpected repairs, moving expenses, and property maintenance can quickly add up. Having adequate reserves demonstrates financial responsibility and may strengthen your mortgage application.

Another common misconception is that first-time home buyers need a 20% down payment. While putting more money down can reduce monthly payments and eliminate private mortgage insurance in some situations, many mortgage programs allow significantly smaller down payments for qualified borrowers.

Which Mortgage Loan Is Best for Borrowers With Student Debt?

There isn’t a single mortgage program that’s perfect for everyone. The ideal choice depends on your income, military status, location, credit score, down payment, and overall financial goals. Comparing available loan options can help borrowers determine which program aligns best with their circumstances.

| Mortgage Program | Minimum Down Payment* | Best For | Student Loan Flexibility |

|---|---|---|---|

| Conventional Loan | As low as 3% | Strong credit borrowers | Depends on lender guidelines |

| FHA Loan | As low as 3.5% | Lower credit scores | Often flexible for qualified borrowers |

| VA Loan | Eligible veterans and service members | No down payment in many cases | Excellent option for eligible military borrowers |

| USDA Loan | Eligible rural buyers | No down payment for qualifying properties | Helpful for eligible low-to-moderate income borrowers |

*Actual eligibility varies by lender and current program requirements.

Conventional Loans

Conventional mortgages remain one of the most popular choices for borrowers with solid credit profiles. They often provide competitive interest rates and flexible loan terms. Many lenders offering conventional loans evaluate student loan payments using current underwriting guidelines, making documentation especially important. Providing accurate repayment information can help ensure your debt-to-income ratio reflects your actual monthly obligations.

FHA Loans

FHA loans are frequently chosen by first-time home buyers because they generally accommodate lower credit scores and smaller down payments than many conventional loans. Borrowers with student debt often appreciate the flexibility available through FHA lending guidelines. Still, lenders may apply additional underwriting standards, sometimes called overlays, beyond the minimum program requirements.

VA Loans

Eligible veterans, active-duty service members, and certain surviving spouses may qualify for VA loans. These mortgages often require no down payment and do not include monthly mortgage insurance, making them particularly attractive for eligible military families. Student loans are still considered during underwriting, but the overall program offers substantial advantages for qualified applicants.

USDA Loans

USDA loans support eligible homebuyers purchasing properties in qualifying rural and suburban areas. They can be an excellent option for borrowers with moderate incomes who meet location and eligibility requirements. Like other mortgage programs, student loan obligations remain part of the underwriting process, but many qualified applicants successfully obtain USDA financing despite carrying education debt.

Can Student Loan Forgiveness Help You Qualify?

Student loan forgiveness can improve mortgage eligibility, but the timing and impact depend on your individual circumstances. If forgiveness permanently eliminates a monthly student loan payment, your debt-to-income ratio may improve considerably. However, borrowers should avoid assuming future forgiveness will automatically influence current mortgage approval.

Most lenders evaluate your financial situation based on documented obligations at the time you apply. If forgiveness has not yet been finalized, the lender may still need to include your existing payment when calculating DTI. Once forgiveness becomes official and your repayment obligation changes, future mortgage applications may reflect the updated financial picture.

Borrowers pursuing forgiveness through qualifying federal programs should maintain complete documentation and communicate any changes to their mortgage lender. Clear records help ensure the lender uses accurate information during underwriting.

Should You Refinance Student Loans Before Buying a Home?

Refinancing can sometimes improve mortgage qualification, but it isn’t always the best decision.

If refinancing lowers your required monthly payment without significantly extending repayment or increasing total borrowing costs, your debt-to-income ratio may improve. This could strengthen your mortgage application. However, refinancing federal student loans into private loans generally means giving up federal benefits, including income-driven repayment plans and certain forgiveness opportunities.

Before refinancing, ask yourself:

- Will my monthly payment actually decrease?

- Am I losing valuable federal protections?

- Will refinancing improve my DTI enough to matter?

- Can I qualify for better interest rates?

Depending on your financial profile, keeping federal repayment benefits may provide more long-term value than achieving a slightly lower monthly payment.

Expert Tips

Expert Tips for Buying a Home With Student Loans

- Check your credit reports several months before applying.

- Avoid opening new credit accounts during the mortgage process.

- Save additional cash beyond your down payment.

- Reduce high-interest debt whenever possible.

- Compare mortgage offers from multiple lenders.

- Obtain a mortgage pre-approval before house hunting.

- Keep documentation for all student loan repayment plans.

- Remember that lender requirements can vary, so verify guidelines before applying.

Key Takeaways

✔ Having student loans does not automatically prevent mortgage approval.

✔ Debt-to-income ratio is usually more important than total student loan balance.

✔ Income-driven repayment plans may help some borrowers qualify.

✔ FHA, VA, USDA, and Conventional loans each have different qualification standards.

✔ Strong credit, stable income, and adequate savings improve approval chances.

✔ Always compare multiple lenders because underwriting policies can differ.

Common Mistakes to Avoid When Applying for a Mortgage With Student Loans

Even financially responsible borrowers make mistakes that can delay mortgage approval or reduce the amount they qualify to borrow. The good news is that most of these issues are preventable with proper planning.

One of the biggest mistakes is assuming that student loan debt automatically disqualifies you from buying a home. Many borrowers postpone homeownership for years because they believe they must completely eliminate their education debt first. In reality, lenders focus on affordability rather than simply looking at your total loan balance.

Another common mistake is applying for new credit shortly before a mortgage application. Financing a new car, opening multiple credit cards, or taking out personal loans can increase your debt-to-income ratio and temporarily affect your credit score. Mortgage lenders prefer to see financial stability throughout the approval process.

Many buyers also skip mortgage pre-approval and begin shopping for homes immediately. Without knowing your realistic borrowing capacity, it’s easy to fall in love with a property that’s outside your budget. A pre-approval provides clarity and demonstrates to sellers that you’re a serious buyer.

Finally, failing to compare lenders can be expensive. Interest rates, closing costs, underwriting standards, and student loan calculations may differ between lenders. Taking time to compare multiple offers could save thousands of dollars over the life of your mortgage.

Pros and Cons of Buying a Home With Student Loan Debt

| Pros | Cons |

|---|---|

| Start building home equity sooner | Higher debt-to-income ratio |

| Continue investing instead of waiting years | May qualify for a smaller mortgage |

| Potential property appreciation | Less monthly financial flexibility |

| Access first-time homebuyer programs | A larger emergency fund may be needed |

| Fixed mortgage payments provide stability | Approval may require stronger credit |

Frequently Asked Questions (FAQs)

1. Can I buy a house if I still owe student loans?

Yes. Many borrowers purchase homes while repaying student loans. Approval depends on your overall financial profile rather than student debt alone.

2. Do student loans lower mortgage approval chances?

They can if they significantly increase your debt-to-income ratio, but they rarely prevent approval by themselves.

3. How much student debt is acceptable for a mortgage?

There is no universal limit. Lenders focus primarily on your required monthly payment and your overall DTI.

4. Do FHA loans calculate student loans differently?

FHA loans follow their own underwriting guidelines, which may differ from conventional loans. Always verify current lender requirements.

5. Can deferred student loans affect mortgage approval?

Yes. Deferred loans are generally still considered during underwriting, although calculation methods vary.

6. Can I get pre-approved for student loans?

Absolutely. Many borrowers receive mortgage pre-approval while actively repaying student loans.

7. Should I pay off student loans before buying a house?

Not necessarily. Depending on your financial goals, saving for a down payment or reducing high-interest debt may provide greater benefits.

8. Will student loan forgiveness improve mortgage eligibility?

If forgiveness permanently reduces your monthly debt obligation, it may improve your debt-to-income ratio.

9. Do private student loans affect mortgage approval?

Yes. Private student loans are included in debt calculations just like most other recurring debts.

10. Does an income-driven repayment plan help qualify?

It may. Lower documented monthly payments can improve your debt-to-income ratio, depending on lender guidelines.

11. Can I qualify with a high DTI ratio?

Some borrowers can, particularly if they have strong credit, significant assets, or other compensating factors.

12. Which mortgage loan is easiest with student debt?

There isn’t one universal answer. FHA, VA, USDA, and Conventional loans all serve different borrower needs.

13. Does refinancing student loans improve mortgage approval?

It can if refinancing meaningfully reduces your required monthly payment without creating new financial disadvantages.

14. Can first-time home buyers qualify with student loans?

Yes. Millions of first-time buyers purchase homes every year while carrying student loan debt.

15. What is the best way to improve mortgage approval chances?

Improve your credit score, reduce debt, increase savings, maintain stable employment, and compare offers from multiple lenders.

Conclusion

Student loan debt does not have to delay your dream of homeownership. While lenders certainly consider your education loans during the mortgage approval process, they also evaluate your income, employment history, credit score, savings, debt-to-income ratio, and overall financial stability. Many first-time home buyers assume they need to eliminate every dollar of student debt before applying, but that simply isn’t true in many situations.

One practical strategy is to prepare several months before applying. Check your credit score, calculate your debt-to-income ratio, organize financial documents, and compare multiple mortgage lenders. If you’re eligible, explore first-time homebuyer assistance programs and government-backed mortgage options. Since lender requirements can vary, always confirm current underwriting guidelines with your chosen lender before submitting an application.

By understanding how mortgage lenders evaluate student loan debt, you’ll be in a much stronger position to make informed financial decisions and confidently begin your journey toward homeownership.