Learn How to Get Pre-Approved for a Mortgage in 2026 with this complete USA guide. Discover credit score requirements, documents, lender comparisons, approval tips, timelines, and common mistakes to avoid.

If you’re planning to buy your first home in the United States, learning How to Get Pre-Approved for a Mortgage in 2026 should be your very first priority. Many first-time buyers spend weeks browsing homes online before speaking with a lender. Unfortunately, that often leads to disappointment when they discover their budget is much lower—or sometimes higher—than expected.

A mortgage pre-approval gives you something far more valuable than an estimate. It provides a lender’s written opinion that you’re likely to qualify for a home loan based on your verified financial information. Sellers also take buyers with a pre-approval letter more seriously, especially in competitive housing markets where multiple offers are common. According to mortgage experts, buyers who already have financing lined up often move through the home-buying process faster because much of the financial review has already been completed.

Whether you’re a first-time home buyer, upgrading to a larger home, or relocating for work, this guide walks through every stage of the mortgage approval process. You’ll learn which documents lenders require, what credit score improves your chances, how debt-to-income ratios affect approval, and the smartest ways to compare lenders without hurting your credit. By the end, you’ll know exactly how to prepare for mortgage approval with confidence.

Why Mortgage Pre-Approval Matters More Than Ever in 2026

Buying a home has always been one of life’s biggest financial decisions, but today’s market makes preparation even more important. Home prices remain elevated in many metropolitan areas, mortgage rates continue to fluctuate, and lenders are carefully evaluating borrower qualifications. That means walking into the market without a pre-approval can put you at a significant disadvantage.

A mortgage pre-approval helps you establish a realistic home-buying budget before emotions take over. Instead of falling in love with properties outside your price range, you’ll know exactly how much financing you’re likely to receive. This saves time, reduces stress, and makes conversations with real estate agents much more productive.

Pre-approval also strengthens your offer. Sellers frequently receive multiple offers, and many prefer buyers who already have financing arranged because it reduces the chance of the sale falling apart later. A pre-approval letter isn’t a final guarantee, but it demonstrates that a lender has already reviewed your income, assets, employment, and credit profile.

What Is Mortgage Pre-Approval?

A mortgage pre-approval is a lender’s conditional commitment stating how much money they may be willing to lend you for a home purchase after reviewing your financial information. Unlike a simple online estimate, this process includes document verification, a review of your debts, employment history, available assets, and typically a hard credit inquiry.

The lender evaluates several important factors:

- Credit score

- Employment history

- Monthly income

- Debt-to-income (DTI) ratio

- Available savings

- Down payment funds

- Existing loans and financial obligations

Once approved, you’ll usually receive a pre approval letter showing the maximum loan amount you qualify for. Most letters remain valid for 60 to 90 days, although policies differ by lender.

Mortgage Prequalification vs. Mortgage Pre-Approval

Many buyers mistakenly believe these two terms mean the same thing. They don’t.

| Feature | Mortgage Prequalification | Mortgage Pre-Approval |

|---|---|---|

| Credit Check | Usually Soft | Usually Hard |

| Income Verification | Self-reported | Verified |

| Documents Required | Few | Extensive |

| Seller Confidence | Low | High |

| Loan Estimate | Usually No | Often Yes |

| Best For | Early planning | House shopping |

Think of prequalification as an estimate and pre-approval as evidence. If you’re serious about buying a home in 2026, pre-approval is the stronger option because it provides much greater credibility with sellers and real estate professionals.

Step 1: Know How Much House You Can Afford

Before filling out any mortgage application, determine a realistic budget. Many buyers focus only on the monthly mortgage payment, but homeownership involves much more than principal and interest.

You’ll also need to budget for:

- Property taxes

- Homeowners insurance

- HOA dues (if applicable)

- Maintenance costs

- Utilities

- Closing costs

- Emergency savings

A lender may approve you for more than you’re personally comfortable borrowing. Just because you qualify doesn’t necessarily mean it’s the smartest financial decision. Consider your lifestyle, career stability, family plans, and future expenses before choosing your price range.

Many financial professionals recommend keeping your total housing expenses manageable relative to your income rather than borrowing the maximum available amount. Using a mortgage calculator before speaking with lenders can help you understand different payment scenarios based on down payment size, interest rate, and loan term.

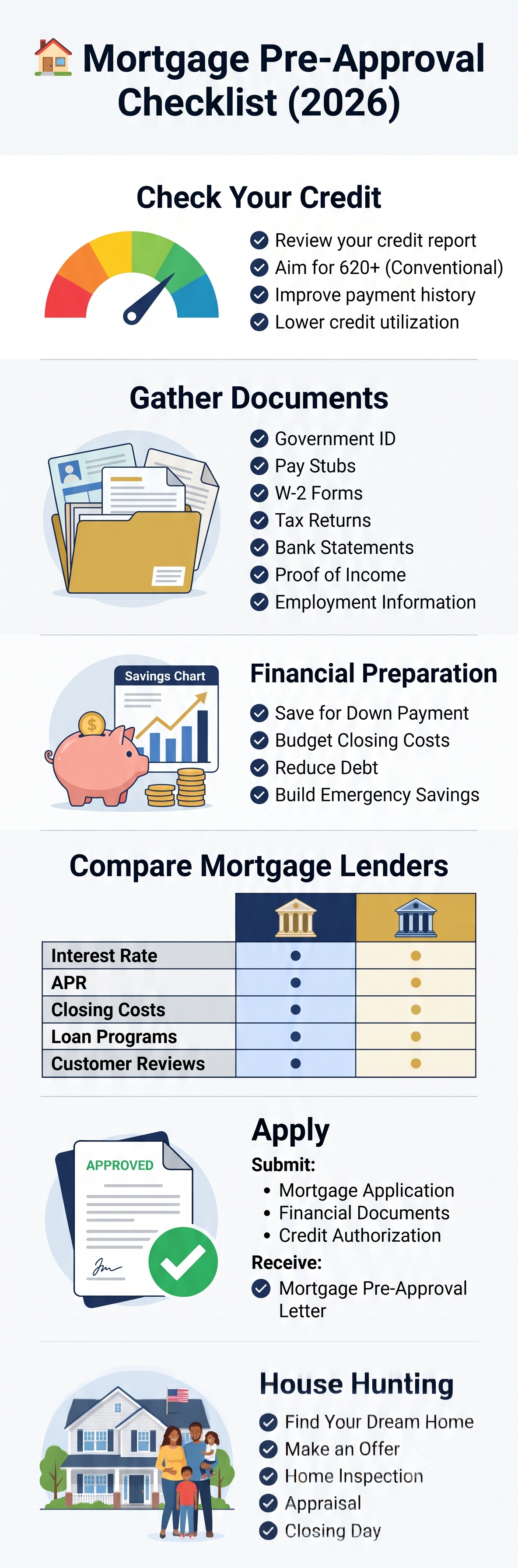

Step 2: Review Your Credit Before Applying

Your credit score remains one of the biggest factors influencing mortgage approval. It doesn’t just determine whether you’ll qualify—it also affects your interest rate, monthly payment, and total borrowing cost over the life of the loan.

Different loan programs have different minimum credit score requirements.

| Loan Type | Typical Minimum Credit Score |

|---|---|

| Conventional Loan | 620+ |

| FHA Loan | 580 (sometimes lower with a larger down payment) |

| VA Loan | Varies by lender |

| USDA Loan | Usually 640+ preferred |

Even if you already meet the minimum requirements, improving your score before applying could save thousands of dollars over the life of your mortgage through lower interest rates. Common ways to improve your credit include paying bills on time, reducing credit card balances, avoiding new debt, and checking your credit report for errors before applying.

Step 3: Gather Every Required Mortgage Document

Once you’ve reviewed your credit and established a realistic budget, it’s time to prepare your paperwork. One of the biggest reasons mortgage applications are delayed isn’t poor credit—it’s incomplete documentation. Lenders need to verify that you have stable income, manageable debt, sufficient savings, and a reliable financial history before issuing a mortgage pre-approval.

Think of this step as preparing for an important job interview. The more organized you are, the smoother the process becomes. Having every document ready before you apply also demonstrates that you’re a serious buyer, allowing your loan officer to review your application faster and reduce unnecessary back-and-forth requests.

While document requirements can vary depending on the lender and loan program, most mortgage lenders in the USA request similar financial records. If you’re self-employed, own a business, or receive commission-based income, expect additional verification requirements because lenders typically need to confirm that your income is stable over time.

Complete Mortgage Document Checklist

Here’s a comprehensive checklist that most lenders request during the mortgage application process.

| Document | Why It’s Required |

|---|---|

| Government-issued ID | Identity verification |

| Social Security Number | Credit and identity checks |

| Recent Pay Stubs | Verify current income |

| W-2 Forms (Last 2 Years) | Employment history |

| Federal Tax Returns | Income verification |

| Bank Statements (2–3 Months) | Cash reserves and spending patterns |

| Investment Statements | Additional assets |

| Retirement Account Statements | Reserve funds |

| Gift Letter (if applicable) | Down payment assistance |

| Rental History | Payment consistency |

| Employer Contact Information | Employment verification |

Self-employed borrowers generally need:

- Two years of business tax returns

- Profit and Loss (P&L) statements

- Business bank statements

- CPA-prepared financial documents (if available)

- Business licenses (sometimes requested)

Preparing these documents before contacting lenders can reduce approval time significantly. Digital copies saved as PDFs are especially helpful because many lenders now offer secure online portals where documents can be uploaded instantly.

Understanding Income Requirements

One of the most common questions from first-time buyers is:

“How much income do I need to buy a home?”

The answer depends on several factors—not just your salary.

Mortgage lenders evaluate:

- Gross monthly income

- Existing monthly debts

- Credit score

- Down payment

- Loan type

- Interest rate

- Property taxes

- Insurance costs

For example, someone earning $70,000 annually with almost no debt may qualify for a larger mortgage than someone earning $90,000 who has significant car loans, student loans, and credit card balances.

Lenders don’t simply look at how much money you make—they examine how much of that income is already committed to existing financial obligations. Stable employment history also plays a major role. Ideally, lenders prefer borrowers who have worked consistently in the same industry for at least two years, although career advancement or changing employers within the same field is often acceptable.

If your income includes bonuses, overtime, commissions, or freelance work, lenders may average those earnings over a two-year period to determine qualifying income.

Debt-to-Income (DTI) Ratio Explained

Your Debt-to-Income Ratio (DTI) is one of the most important numbers in the entire mortgage approval process.

It tells lenders how much of your monthly income already goes toward debt payments.

The basic formula is simple:

Monthly Debt Payments ÷ Gross Monthly Income × 100 = DTI Ratio

For example:

Monthly Income: $6,000

Monthly Debt:

- Car Loan: $350

- Student Loan: $250

- Credit Cards: $200

Total Debt = $800

DTI = 13.3%

Now let’s compare different DTI levels.

| DTI Ratio | General Interpretation |

|---|---|

| Under 36% | Excellent |

| 36%–43% | Good |

| 43%–50% | May still qualify with some programs |

| Above 50% | Approval becomes more difficult |

Many conventional loans prefer a DTI below 43%, although certain government-backed programs may allow higher ratios depending on compensating factors such as strong credit or significant savings.

Reducing your DTI before applying can dramatically improve your approval odds. Paying off smaller credit card balances, avoiding new financing, and increasing your monthly income are all strategies that may strengthen your application.

Employment Verification: Why It Matters

Even borrowers with outstanding credit scores can experience delays if employment cannot be verified.

Most lenders confirm:

- Current employer

- Position

- Employment status

- Salary

- Length of employment

Verification usually occurs more than once.

Many buyers don’t realize lenders often perform a final employment verification just days before closing. Quitting your job, switching employers unexpectedly, or moving from salaried employment to self-employment during the mortgage process can create significant complications.

If you’re planning a career change, it’s generally wise to discuss timing with your loan officer before making any major employment decisions.

Consistency and stability are key factors lenders value because they reduce lending risk.

How Much Money Should You Save Before Applying?

Saving for a home involves much more than accumulating a down payment.

Many first-time buyers underestimate the total amount they’ll need at closing.

Your savings should ideally cover:

- Down payment

- Closing costs

- Earnest money deposit

- Moving expenses

- Initial repairs

- Emergency fund

- Furniture and appliances

Having additional reserves beyond the minimum required amount can also strengthen your mortgage application because it demonstrates financial stability.

For example, if unexpected repairs arise shortly after moving in, emergency savings help prevent financial hardship.

Down Payment Explained

The down payment is your upfront contribution toward the purchase price of the home.

Contrary to popular belief, you don’t always need 20%.

Typical minimum down payments include:

| Loan Type | Typical Minimum Down Payment |

|---|---|

| Conventional Loan | 3%–5% |

| FHA Loan | 3.5% |

| VA Loan | 0% (Eligible Veterans) |

| USDA Loan | 0% (Eligible Rural Areas) |

While a larger down payment can reduce monthly payments and eliminate Private Mortgage Insurance (PMI) in some cases, waiting years to save 20% isn’t always the best strategy if home prices continue rising.

Many first-time buyers successfully purchase homes with much smaller down payments using government-backed loan programs.

Choosing the Right Mortgage Lender

Not every lender offers the same rates, fees, customer service, or loan products.

Shopping around can potentially save thousands of dollars over the life of your loan.

Consider comparing:

- Interest rates

- Origination fees

- Closing costs

- Loan programs

- Customer reviews

- Average closing time

- Digital application tools

- Communication quality

Remember, the lender advertising the lowest interest rate isn’t always the least expensive overall. Closing costs and lender fees should also be carefully reviewed.

Banks vs Credit Unions vs Online Mortgage Lenders

Each lender type has advantages.

| Lender Type | Advantages | Possible Drawbacks |

|---|---|---|

| Traditional Banks | Familiar, multiple financial services | Sometimes slower approvals |

| Credit Unions | Competitive rates, personalized service | Membership may be required |

| Online Lenders | Fast approvals, digital convenience | Less face-to-face interaction |

| Mortgage Brokers | Compare multiple lenders | Broker fees may apply |

For most first-time buyers, obtaining Loan Estimates from at least three lenders provides a clearer picture of available financing options.

Comparing Loan Estimates

After submitting your application, lenders provide a Loan Estimate, which outlines the expected costs associated with your mortgage.

Instead of focusing only on the advertised interest rate, compare:

- Interest Rate

- APR (Annual Percentage Rate)

- Monthly Payment

- Closing Costs

- Origination Charges

- Discount Points

- PMI Costs

- Estimated Cash to Close

Sample Loan Comparison

| Feature | Lender A | Lender B | Lender C |

|---|---|---|---|

| Interest Rate | 6.25% | 6.35% | 6.18% |

| APR | 6.42% | 6.39% | 6.40% |

| Closing Costs | $6,800 | $5,900 | $7,200 |

| PMI | Lower | Medium | Higher |

| Estimated Closing Time | 25 Days | 30 Days | 22 Days |

A slightly higher interest rate paired with lower closing costs may actually be the better financial choice, depending on how long you plan to own the home.

Don’t hesitate to ask lenders to explain every fee. Understanding the full cost of borrowing helps you make an informed decision rather than choosing based solely on the advertised rate.

Step 5: Submit Your Mortgage Application

After you’ve selected a lender and gathered all your financial documents, it’s time to officially submit your mortgage application. This is where the pre-approval process becomes more detailed. Your lender will carefully review your financial profile, verify the information you’ve provided, and determine whether you meet the requirements for the loan program you’ve chosen.

Most lenders today offer online applications, making the process faster and more convenient than ever. You’ll typically provide personal information, employment history, income details, assets, debts, and permission for the lender to check your credit. Accuracy is essential. Even small mistakes—such as entering an incorrect salary, forgetting an existing loan, or omitting a bank account—can delay your application or require additional documentation later.

After receiving your application, the lender usually reviews it within a few business days. If everything looks good, you’ll receive a pre approval letter, which states the estimated loan amount you qualify for. This letter becomes one of your strongest tools when shopping for a home because sellers know you’ve already completed an important part of the financing process. Keep in mind, however, that a pre-approval is conditional. Final approval still depends on the property you choose, a successful appraisal, updated financial verification, and the underwriting process.

Step 6: Mortgage Underwriting Explained

Many first-time buyers hear the word underwriting and immediately assume something has gone wrong. In reality, underwriting is a standard part of every mortgage transaction. It’s simply the lender’s way of performing a final review before committing to lend hundreds of thousands of dollars.

An underwriter acts as the lender’s risk evaluator. They verify that your financial information is accurate, confirm your employment and income, review your credit history, analyze your debt-to-income ratio, and ensure the property itself meets lending guidelines. Even if you’ve already received a pre-approval, the underwriter performs an independent review to confirm that nothing has changed.

During underwriting, you may receive requests for additional documents. This is perfectly normal. The lender might ask for updated pay stubs, recent bank statements, explanations for large deposits, or clarification regarding credit inquiries. Responding quickly helps keep your loan on schedule. Delays usually occur when borrowers take several days to provide requested information or submit incomplete documents.

At the end of underwriting, one of three outcomes generally occurs:

- Approved

- Approved with conditions

- Denied

An approval with conditions is the most common result. It simply means the lender needs one or two additional items before issuing final approval.

Comparing Popular Mortgage Loan Types

Choosing the right loan program is just as important as choosing the right lender. Different loans serve different types of borrowers, and understanding their requirements can help you make a smarter financial decision.

| Feature | FHA Loan | Conventional Loan | VA Loan | USDA Loan |

|---|---|---|---|---|

| Minimum Down Payment | 3.5% | 3–5% | 0% | 0% |

| Credit Score | 580+ typical | 620+ typical | Varies | Usually 640+ preferred |

| Mortgage Insurance | Required | Required if under 20% down | None | Guarantee Fee |

| Best For | First-time buyers | Strong credit borrowers | Eligible veterans and service members | Rural home buyers |

| Property Restrictions | Standard | Standard | Primary residence | Eligible rural areas |

FHA Loans

FHA loans are popular among first-time home buyers because they require lower down payments and are generally more forgiving of lower credit scores. However, borrowers must pay mortgage insurance premiums, which increase the overall cost of the loan.

Conventional Loans

Conventional loans often provide lower long-term costs for borrowers with strong credit. If you can put down at least 20%, you may avoid Private Mortgage Insurance (PMI), reducing your monthly payment.

VA Loans

VA loans offer exceptional benefits to eligible veterans, active-duty military personnel, and certain surviving spouses. They often require no down payment and no monthly mortgage insurance, making them one of the most affordable financing options available.

USDA Loans

USDA loans help eligible borrowers purchase homes in designated rural and suburban areas. Qualified buyers may receive 100% financing, although income limits and property eligibility requirements apply.

Mortgage Approval Timeline

Many buyers wonder how long the mortgage process actually takes. While every situation is unique, understanding the typical timeline helps set realistic expectations.

| Stage | Estimated Time |

|---|---|

| Credit Review | Same Day–2 Days |

| Submit Documents | 1–3 Days |

| Mortgage Pre-Approval | 1–7 Days |

| House Hunting | Several Weeks to Several Months |

| Purchase Agreement | 1–3 Days |

| Home Inspection | About 1 Week |

| Appraisal | 1–2 Weeks |

| Underwriting | 1–3 Weeks |

| Final Approval | 1–3 Days |

| Closing | Usually 30–45 Days After Offer Acceptance |

The timeline can move much faster if your paperwork is organized and the property appraisal doesn’t encounter issues. Conversely, incomplete documents, employment changes, appraisal delays, or title problems can extend the process.

Common Mistakes That Delay Mortgage Approval

Even financially qualified borrowers sometimes experience unnecessary delays because of avoidable mistakes. Being aware of these issues can save both time and frustration.

| Mistake | Potential Impact |

|---|---|

| Applying for new credit cards | Increases debt and triggers additional credit checks |

| Financing a new vehicle | Raises the DTI ratio |

| Missing bill payments | Lowers credit score |

| Large unexplained bank deposits | Requires additional documentation |

| Changing jobs | May require new employment verification |

| Making large purchases | Reduces available cash reserves |

| Closing old credit accounts | Can a lower credit score |

| Ignoring lender requests | Delays underwriting |

One common misconception is that once you’re pre-approved, your finances no longer matter. That’s simply not true. Lenders continue monitoring your financial profile throughout the mortgage process. Maintaining financial stability until closing is one of the smartest things you can do.

How to Improve Your Mortgage Approval Chances?

Getting pre-approved isn’t just about meeting the minimum requirements. Strong applicants often enjoy better interest rates, lower monthly payments, and a smoother approval process.

Consider these practical strategies:

Improve Your Credit Score

Pay every bill on time, reduce revolving credit card balances, avoid opening unnecessary accounts, and review your credit report for errors before applying.

Lower Your Debt

Paying off high-interest credit cards or personal loans can significantly improve your debt-to-income ratio, making you a more attractive borrower.

Increase Your Savings

Lenders like to see borrowers with cash reserves. Beyond your down payment, having emergency savings demonstrates financial responsibility.

Maintain Stable Employment

Avoid changing jobs during the application process unless absolutely necessary. Stability gives lenders greater confidence in your ability to repay the loan.

Compare Multiple Lenders

Interest rates and closing costs vary widely. Requesting Loan Estimates from several lenders allows you to compare offers and negotiate better terms.

Avoid Major Financial Changes

Postpone purchasing furniture, electronics, or vehicles until after closing. Keeping your finances consistent helps prevent last-minute complications.

Real-World Example: Sarah’s First Home Purchase

Sarah, a 29-year-old marketing specialist, wanted to buy her first home in Texas. Initially, she planned to start touring homes immediately, but her real estate agent recommended obtaining a mortgage pre-approval first.

After reviewing her finances, Sarah discovered her credit score was 648. Rather than applying immediately, she spent three months paying down credit card balances and correcting an error on her credit report. Her score increased to 703.

She also compared four lenders instead of accepting the first offer she received. One lender offered a slightly lower interest rate but much higher closing costs. Another offered a competitive rate with lower fees and faster closing times.

Because Sarah entered the market with a strong pre-approval, organized documents, and realistic expectations, her offer stood out in a competitive bidding situation. She closed on her first home in just over a month without unexpected financing issues.

Her experience highlights an important lesson: preparation often saves far more money than rushing into the process.

Expert Tips for First-Time Home Buyers

Experienced mortgage professionals consistently recommend a few best practices that can make the entire journey smoother:

- Start preparing your finances several months before applying.

- Review your credit report early so you have time to correct mistakes.

- Save more than just the minimum down payment.

- Don’t focus solely on the interest rate—compare total loan costs.

- Keep detailed financial records in one secure location.

- Ask questions whenever you don’t understand lender terminology.

- Stay financially consistent until after closing.

- Work with professionals who communicate clearly and respond promptly.

Buying your first home can feel overwhelming, but careful planning transforms a complicated process into a manageable series of steps. The better prepared you are before applying, the more confidence you’ll have throughout your home-buying journey.

What Happens After You Get Pre-Approved?

Receiving your mortgage pre-approval is an exciting milestone, but it doesn’t mean your mortgage is fully approved. Think of pre-approval as your ticket to start shopping for a home with confidence. It tells sellers and real estate agents that a lender has reviewed your financial profile and believes you qualify for a loan under current conditions.

Once you have your pre-approval letter, you can begin touring homes within your approved price range. When you find the right property, you’ll submit an offer. If the seller accepts, your lender will move forward with the full mortgage process, which includes ordering a home appraisal, verifying your financial information again, and completing underwriting.

During this period, it’s essential to maintain your financial stability. Continue making all payments on time, avoid taking on new debt, and don’t make major purchases like cars or expensive furniture. Lenders often perform one final review before closing, and any significant financial changes could affect your loan approval.

When Should You Renew Your Mortgage Pre-Approval?

Most mortgage pre-approval letters remain valid for 60 to 90 days, although the exact timeframe depends on the lender.

If your home search takes longer than expected, don’t panic. Renewing your pre-approval is usually a straightforward process. Your lender may ask for updated documents, such as recent pay stubs, bank statements, or a refreshed credit check, to confirm that your financial situation hasn’t changed.

Renewing your pre-approval helps ensure that your loan amount still reflects current interest rates, lending guidelines, and your financial circumstances. It’s especially important in a changing housing market where rates and affordability can shift over time.

Can You Be Denied After Being Pre-Approved?

Yes—but it’s less likely if your financial situation remains stable.

Some common reasons a borrower may be denied after receiving a pre-approval include:

- Losing or changing jobs without informing the lender.

- Taking on significant new debt.

- Missing payments that lower your credit score.

- Providing inaccurate information during the application.

- The home appraisal is coming in below the purchase price.

- Issues discovered during underwriting, such as undisclosed liabilities or unverifiable income.

The good news is that most of these situations are preventable. By staying financially consistent and responding promptly to lender requests, you can significantly reduce the chances of unexpected problems before closing.

Final Thoughts

Learning how to Get Pre-Approved for a Mortgage in 2026 is one of the smartest steps you can take before beginning your home-buying journey. A mortgage pre-approval not only helps you understand your budget but also strengthens your position when competing for homes in today’s market.

Success comes down to preparation. Review your credit, organize your financial documents, calculate your debt-to-income ratio, compare multiple lenders, and avoid unnecessary financial changes while your application is in progress. These simple but effective steps can improve your approval odds and help you secure better loan terms.

Whether you’re a first-time home buyer or purchasing another property, taking the time to prepare before applying can save money, reduce stress, and make the entire process much smoother. A little planning today can make all the difference when it’s time to unlock the front door of your new home.

Frequently Asked Questions (FAQs)

1. What is mortgage pre-approval?

Mortgage pre-approval is a lender’s conditional commitment stating how much you may be able to borrow after reviewing your income, credit, assets, and financial documents. It gives sellers confidence that you’re a qualified buyer.

2. How long does mortgage pre-approval last?

Most pre-approval letters are valid for 60 to 90 days. If you haven’t purchased a home by then, your lender can usually renew the pre-approval after reviewing updated financial information.

3. Does getting pre-approved affect my credit score?

Yes. Most lenders perform a hard credit inquiry, which may temporarily reduce your credit score by a few points. Shopping with multiple mortgage lenders within a short period is generally treated as a single inquiry by many credit scoring models.

4. What credit score is needed for mortgage pre-approval?

Requirements vary by loan program. Conventional loans typically require a score of 620 or higher, while FHA loans may allow lower scores if other qualifications are met.

5. Should I get pre-approved before looking at homes?

Absolutely. Getting pre-approved before house hunting helps you understand your budget, strengthens your purchase offer, and prevents you from falling in love with homes outside your price range.