Learn what a good debt-to-income ratio for a mortgage is, how lenders calculate DTI, ideal ranges, loan requirements, and tips to improve your approval chances.

Buying a home is exciting until the mortgage application asks questions you weren’t expecting. One number that surprises many first-time buyers is the debt-to-income ratio (DTI). You may have an excellent credit score, stable employment, and enough savings for a down payment, yet your mortgage approval can still depend heavily on this single financial metric.

If you’ve been asking “What Is a Good Debt-to-Income Ratio for a Mortgage?”, you’re asking one of the most important questions in the home-buying process. Mortgage lenders use your debt-to-income ratio to determine whether you can comfortably afford another monthly payment without creating excessive financial risk. A lower DTI tells lenders you have room in your budget, while a higher DTI suggests your income may already be stretched.

Although DTI is extremely important, it isn’t the only factor lenders consider. Your credit score, employment history, available cash reserves, down payment, and loan program also influence approval decisions. Many conventional lenders prefer borrowers with a back-end DTI below 36%, but some government-backed loan programs may approve significantly higher ratios when other parts of your financial profile are strong.

What is The Debt-to-Income Ratio?

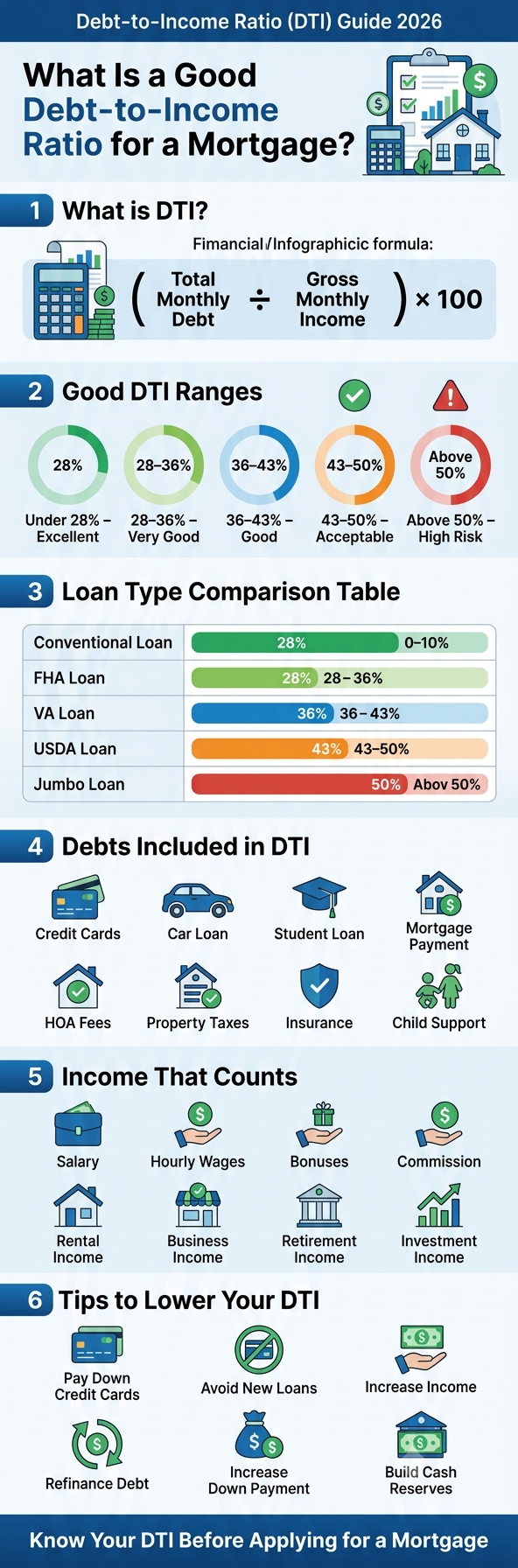

Your Debt-to-Income Ratio (DTI) is the percentage of your gross monthly income that goes toward paying recurring monthly debts. Think of it as a snapshot showing lenders how much of your paycheck is already committed before taking on a new mortgage.

The calculation is straightforward:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

For example:

| Monthly Income | Monthly Debt | DTI |

|---|---|---|

| $6,000 | $1,800 | 30% |

| $8,000 | $3,200 | 40% |

| $5,000 | $2,500 | 50% |

A borrower earning $6,000 per month before taxes who pays $1,800 toward debt has a 30% DTI. That generally falls within the range most lenders consider financially healthy.

What Is Front-End DTI?

The front-end DTI, sometimes called the housing ratio, measures only your housing-related expenses.

These include:

- Mortgage principal

- Interest

- Property taxes

- Homeowners insurance

- HOA dues

- Mortgage insurance (PMI or MIP)

Many conventional lending guidelines historically view 28% as an excellent front-end ratio, though automated underwriting systems may approve higher figures depending on the borrower’s overall profile.

What Is The Back-End DTI?

The back-end DTI is the ratio lenders care about most.

It includes:

- Housing payment

- Credit card minimum payments

- Auto loans

- Student loans

- Personal loans

- Child support

- Alimony

- Other recurring obligations

This ratio provides a more complete picture of your financial commitments because it reflects all required monthly debt payments, not just housing expenses.

Why Does the Debt-to-Income Ratio Matter for Mortgage Approval?

Imagine two borrowers each earning $7,000 per month.

Borrower A owes $700 every month.

Borrower B owes $2,900 every month.

Although both earn exactly the same salary, Borrower A has significantly more financial flexibility. If an unexpected medical bill or car repair appears, Borrower A is more likely to continue making mortgage payments without difficulty.

That’s exactly why lenders evaluate DTI so carefully.

Mortgage underwriting is built around risk management. Every lender wants confidence that borrowers can continue paying their mortgage even if expenses increase or income temporarily declines.

A lower DTI generally means:

- Higher approval odds

- More loan options

- Better mortgage rates

- Lower lender risk

- Greater affordability

A high DTI doesn’t automatically result in denial. Government-backed programs, particularly FHA loans and some VA loans, often permit higher ratios when supported by strong credit scores, substantial savings, or other compensating factors. Individual lenders may also apply stricter standards than program minimums, so approval requirements vary.

Expert Tip: Think of DTI as a financial stress test. The less of your income already committed to debt, the easier it is to absorb life’s unexpected expenses while staying current on your mortgage.

What Is Considered a Good Debt-to-Income Ratio?

Although every lender has different underwriting guidelines, the following ranges are commonly used when evaluating mortgage applicants.

| Debt-to-Income Ratio | Mortgage Assessment |

|---|---|

| Below 28% | Excellent |

| 28%–36% | Very Good |

| 36%–43% | Good |

| 43%–50% | Acceptable for many programs |

| Above 50% | Difficult to qualify |

Below 28%

This is considered an outstanding financial position.

Borrowers in this category generally have plenty of room in their monthly budget, making them attractive applicants. They often receive access to more competitive mortgage products and stronger interest-rate offers when other factors, such as credit score and down payment, are also favorable.

28%–36%

This range is widely viewed as ideal.

Many financial planners recommend keeping total monthly debt below 36% of gross income, and numerous mortgage lenders also consider this a strong benchmark. Applicants within this range typically qualify comfortably for conventional financing, assuming they meet other underwriting requirements.

36%–43%

Borrowers here remain competitive, although lenders may take a closer look at compensating factors such as credit history, employment stability, cash reserves, and loan-to-value ratio.

43%–50%

Approval is still possible, especially through FHA, VA, or certain conventional automated underwriting systems. However, borrowers may face more documentation requests or lender-specific overlays.

Above 50%

Qualifying becomes significantly more challenging.

Some specialized programs and exceptional borrower profiles may still receive approval, but many lenders will recommend reducing monthly debt or increasing documented income before proceeding.

Quick DTI Summary

- ✅ Excellent DTI: Under 28%

- ✅ Ideal DTI: Under 36%

- ✅ Generally Acceptable: Up to 43%

- ✅ Possible With Certain Loan Programs: 43–50%

- ✅ High Risk: Above 50%

Maximum Debt-to-Income Ratio by Loan Type

One of the biggest misconceptions among homebuyers is that every mortgage program follows the same DTI requirements. In reality, each loan type has its own underwriting guidelines, and individual lenders may also impose stricter “overlays” than the minimum standards set by the loan program. That’s why two borrowers with identical incomes and debt levels may receive different approval decisions depending on the lender and the mortgage product they choose.

While a lower DTI always strengthens your mortgage application, many government-backed loans are designed to help borrowers qualify with slightly higher debt levels if they demonstrate strong compensating factors, such as a solid credit history, stable employment, cash reserves, or a larger down payment.

Maximum Debt-to-Income Ratio Comparison

| Loan Type | Preferred DTI | Maximum DTI (Typical) | Notes |

|---|---|---|---|

| Conventional Loan | Below 36% | Up to 45% (sometimes higher with automated underwriting) | Strong credit improves approval odds. |

| FHA Loan | Below 43% | Up to 57% in some approved cases | Flexible guidelines for first-time buyers. |

| VA Loan | Around 41% benchmark | Higher possible with compensating factors | Focuses on overall residual income, not just DTI. |

| USDA Loan | Around 41% | Higher with strong application | Rural property eligibility required. |

| Jumbo Loan | Below 36% | Usually 43% or less | Stricter underwriting due to larger loan amounts. |

Important Note: These are common industry guidelines, not guaranteed approval limits. Every lender evaluates applications differently, and underwriting decisions are based on your complete financial profile.

Conventional Loans

Conventional mortgages, backed by Fannie Mae and Freddie Mac, generally favor borrowers with lower debt obligations. A DTI below 36% is considered excellent, while many borrowers can still qualify with ratios up to 45% through automated underwriting systems if they have strong credit scores, consistent income, and adequate reserves.

For example, a borrower with a 780 FICO Score, stable employment, and a 20% down payment may receive approval with a higher DTI than someone with a lower credit score and minimal savings.

FHA Loans

FHA loans remain one of the most flexible mortgage options available, making them especially popular among first-time homebuyers and borrowers rebuilding their credit.

Although 43% is often referenced as a benchmark, many approved FHA borrowers have significantly higher DTIs when they demonstrate compensating strengths, such as:

- Higher credit scores

- Stable employment history

- Larger savings

- Additional cash reserves

- Significant down payment

This flexibility explains why FHA financing continues to help borrowers who might not qualify for conventional financing.

VA Loans

VA loans are unique because they don’t rely solely on DTI.

Instead, lenders also evaluate Residual Income, which measures how much money remains after all monthly obligations are paid.

A borrower with a slightly higher DTI may still qualify if enough income remains to comfortably cover everyday living expenses. This approach often makes VA loans one of the most flexible mortgage products available for eligible veterans and active-duty service members.

USDA Loans

USDA Rural Development loans are designed for eligible rural and suburban homebuyers.

Most lenders prefer a DTI near 41%, although approvals above this level are possible when borrowers demonstrate strong compensating factors.

Because USDA loans emphasize affordable housing, lenders carefully evaluate whether applicants can comfortably manage long-term mortgage payments.

Jumbo Loans

Jumbo mortgages involve larger loan amounts that exceed conforming loan limits.

Since these loans represent greater financial risk for lenders, underwriting standards are generally stricter.

Most jumbo lenders prefer:

- Excellent credit

- Large down payment

- Significant cash reserves

- Stable employment

- Lower debt-to-income ratio

Many jumbo borrowers find it easier to qualify when their DTI remains below 36%.

How Mortgage Lenders Calculate Debt-to-Income Ratio?

Many borrowers assume DTI calculations are complicated, but the formula itself is surprisingly simple.

The Formula

Debt-to-Income Ratio = Total Monthly Debt Payments ÷ Gross Monthly Income × 100

Remember that lenders always use gross monthly income, meaning income before taxes and deductions.

Example 1

Monthly Income

$6,500

Monthly Debts

Mortgage Payment: $1,600

Car Loan: $400

Student Loan: $250

Credit Card Minimums: $150

Personal Loan: $200

Total Debt = $2,600

DTI Calculation:

$2,600 ÷ $6,500 × 100

= 40%

This borrower falls within the range where many mortgage programs may still approve financing.

Example 2

Monthly Income:

$8,000

Monthly Debt:

Mortgage Payment: $1,800

Car Loan: $300

Credit Cards: $100

Student Loan: $200

Total Debt = $2,400

DTI:

$2,400 ÷ $8,000 ×100

= 30%

This represents a very healthy debt-to-income ratio that many lenders view favorably.

Example 3

Monthly Income:

$5,500

Monthly Debt:

Mortgage = $2,000

Auto Loan = $550

Student Loans = $500

Credit Cards = $300

Personal Loan = $250

Total Debt = $3,600

DTI:

$3,600 ÷ $5,500 ×100

= 65%

This applicant would likely need to reduce debt, increase documented income, or explore alternative financing before qualifying.

Expert Tip

Before applying for a mortgage, calculate your own DTI using realistic monthly obligations rather than estimates. A small overlooked payment can sometimes change underwriting results.

Which Debts Count Toward Your DTI?

One of the biggest misunderstandings during mortgage applications is believing that only loans currently in repayment count toward DTI.

Mortgage lenders actually review nearly every recurring monthly debt obligation that appears on your credit report or must legally be paid each month.

Debts That Usually Count

- ✅ Mortgage payments

- ✅ Rent (in certain situations)

- ✅ Property taxes

- ✅ Homeowners insurance

- ✅ HOA dues

- ✅ Mortgage insurance

- ✅ Auto loans

- ✅ Student loans

- ✅ Personal loans

- ✅ Credit card minimum payments

- ✅ Home equity loans

- ✅ Home equity lines of credit (HELOC)

- ✅ Child support

- ✅ Alimony

- ✅ Installment loans

These obligations directly affect how much money remains available each month for a new mortgage payment.

Debts That Usually Do NOT Count

Most lenders generally do not include:

- Utility bills

- Internet service

- Cell phone bills

- Health insurance premiums

- Groceries

- Gasoline

- Entertainment expenses

- Streaming subscriptions

- Clothing purchases

Although these expenses affect your personal budget, they are typically not considered recurring debt obligations under mortgage underwriting guidelines.

Real-Life Example

Sarah earns $7,000 per month.

She has:

- Car Loan: $420

- Student Loan: $280

- Credit Card Minimums: $180

- Estimated Mortgage Payment: $1,950

- HOA Fee: $150

Her total monthly debt obligations equal:

$2,980

DTI:

$2,980 ÷ $7,000 ×100

= 42.6%

While this is higher than many borrowers expect, Sarah may still qualify depending on her credit score, down payment, loan type, and lender guidelines.

What Income Counts?

Income is just as important as debt when calculating DTI.

Mortgage lenders don’t simply ask how much money you make—they evaluate whether your income is stable, reliable, and likely to continue.

Common Income Sources Accepted

Most lenders may consider:

- Salary

- Hourly wages

- Over time (when consistent)

- Bonuses

- Commission income

- Self-employment income

- Business income

- Rental income

- Retirement income

- Pension benefits

- Social Security income

- Disability benefits (when eligible)

- Military income

- Investment income (when documented)

Each income source must generally meet documentation and continuity requirements.

Self-Employment Income

Self-employed borrowers often undergo additional documentation because income can fluctuate.

Lenders commonly request:

- Two years of tax returns

- Profit and Loss statements

- Business bank statements

- Business licenses

- CPA documentation (when applicable)

Although self-employment isn’t a disadvantage, consistent documented earnings are essential.

Income That May Not Qualify

Temporary or inconsistent income may not always be counted, including:

- One-time bonuses

- Irregular freelance earnings

- Unverified cash payments

- Temporary side jobs

- Income without supporting documentation

Mortgage lenders focus on income they believe will continue after the loan closes.

Quick Summary Box

- ✔ Lower DTI generally improves mortgage approval chances.

- ✔ Government-backed loans often allow higher DTIs than conventional loans.

- ✔ Both debt and verified income determine your DTI.

- ✔ Every lender may apply different underwriting standards.

- ✔ Improving either your income or reducing debt can strengthen your mortgage application.

How To Improve Your Debt-to-Income Ratio Before Applying for a Mortgage?

A high debt-to-income ratio (DTI) doesn’t necessarily mean you have to postpone your dream of buying a home. In many cases, small financial improvements made over several months can significantly strengthen your mortgage application. Since DTI compares your monthly debt obligations to your gross monthly income, improving either side of that equation can work in your favor.

Lenders prefer borrowers who demonstrate financial stability rather than simply high incomes. Someone earning $80,000 annually with very little debt may appear less risky than someone earning $150,000 but carrying substantial monthly loan payments. Before applying for a mortgage, take time to review your financial picture and identify areas where you can reduce obligations or increase verifiable income.

1. Pay Down High-Interest Debt First

One of the fastest ways to improve your DTI is to reduce debts that require monthly payments.

Focus on debts such as:

- Credit cards

- Personal loans

- Auto loans

- Lines of credit

Credit card balances deserve special attention because paying them down can improve both your DTI and your credit utilization ratio, potentially boosting your credit score at the same time.

Example

Current monthly debts:

- Credit Card Minimum: $220

- Personal Loan: $180

- Car Loan: $410

Total Monthly Debt = $810

If you completely pay off the credit card, your monthly debt falls to $590, instantly lowering your DTI without increasing your income.

2. Avoid Taking on New Debt

Many borrowers unknowingly hurt their mortgage application by financing furniture, purchasing a new vehicle, or opening additional credit cards shortly before closing on a home.

Even if you’re already pre-approved, lenders often perform a final credit review before funding your mortgage. A new loan can increase your DTI and potentially change the underwriting decision.

Avoid Before Closing

- New car loans

- Furniture financing

- Buy Now, Pay Later accounts

- Large personal loans

- Multiple new credit card applications

Expert Tip: Delay major purchases until after your mortgage has officially closed.

3. Increase Your Verifiable Income

Improving the income side of the DTI formula can be just as effective as reducing debt.

Depending on your situation, lenders may consider:

- Salary increases

- Consistent overtime

- Bonus income

- Commission income

- Self-employment income

- Rental income

- Retirement benefits

- Investment income

Remember that income usually needs to be documented and expected to continue. Temporary earnings or undocumented cash payments generally won’t strengthen your mortgage application.

4. Increase Your Down Payment

Although a larger down payment doesn’t directly lower your DTI, it reduces the amount you need to borrow.

A smaller mortgage may result in:

- Lower monthly principal and interest payments

- Lower mortgage insurance costs

- Better loan options

- Lower overall monthly housing expenses

This indirectly improves your housing ratio and can make your application more attractive to lenders.

5. Refinance Existing Debt

If interest rates or your financial profile has improved since taking out earlier loans, refinancing could reduce your required monthly payments.

For example:

- Original Car Payment: $620

- Refinanced Payment: $410

- Monthly savings: $210

That reduction immediately lowers your DTI calculation.

Always compare refinancing costs with long-term savings before proceeding.

6. Increase Cash Reserves

Cash reserves don’t change your DTI calculation, but they can strengthen your overall mortgage application.

Many lenders view emergency savings as evidence that you’ll be able to continue making mortgage payments during unexpected financial challenges.

Examples of acceptable reserves include:

- Savings accounts

- Money market accounts

- Certificates of Deposit (CDs)

- Retirement accounts (depending on the loan program)

7. Choose a Less Expensive Home

Sometimes improving your DTI is as simple as reducing the monthly mortgage payment you’re targeting.

A slightly lower purchase price can reduce:

- Principal

- Interest

- Property taxes

- Homeowners insurance

- Mortgage insurance

Those lower housing costs translate into a healthier debt-to-income ratio.

Expert Tip

Don’t focus solely on getting approved.

Choose a mortgage payment that leaves room in your monthly budget for emergencies, retirement savings, home maintenance, vacations, and unexpected expenses. Buying the most expensive home you qualify for isn’t always the smartest long-term financial decision.

Common DTI Mistakes That Can Hurt Mortgage Approval

Even financially responsible borrowers make mistakes that increase their debt-to-income ratio or complicate the underwriting process. Understanding these common pitfalls can improve your approval chances.

Mistake 1: Only Looking at Credit Score

Many buyers believe a high credit score guarantees mortgage approval.

While excellent credit certainly helps, lenders evaluate:

- DTI

- Income stability

- Employment history

- Down payment

- Assets

- Cash reserves

- Loan type

A borrower with a 780 credit score can still be denied if their DTI is excessively high.

Mistake 2: Forgetting Monthly Obligations

Some applicants forget to include:

- Student loans

- Child support

- HOA fees

- Personal loans

- Minimum credit card payments

Mortgage underwriters review your credit report and financial documents carefully, so undisclosed obligations rarely go unnoticed.

Mistake 3: Applying Before Paying Off Debt

If you’re only a few months away from eliminating a major loan payment, waiting could significantly improve your mortgage application.

For example:

Car payment ending in three months: $520/month

Waiting until the loan is paid off could substantially reduce your DTI.

Mistake 4: Opening New Credit Accounts

Applying for financing shortly before mortgage approval creates unnecessary risk.

Examples include:

- New furniture financing

- Electronics financing

- Additional credit cards

- Personal loans

These accounts may increase both your debt and the number of recent credit inquiries.

Mistake 5: Changing Jobs During Underwriting

Changing employers isn’t automatically a problem, but unexpected employment changes can delay verification or require additional documentation.

If possible, avoid changing jobs until after your mortgage closes unless the move clearly strengthens your employment stability.

Mistake 6: Ignoring Student Loans

Many borrowers mistakenly assume deferred student loans don’t affect mortgage approval.

Depending on the loan program, lenders may still include a calculated monthly payment when determining DTI.

Mistake 7: Overestimating Future Income

Mortgage approval relies on documented, verifiable income—not expected raises or anticipated bonuses.

Underwriters focus on income that can be reasonably verified and is expected to continue.

Myth vs. Fact

| Myth | Fact |

|---|---|

| A high credit score guarantees mortgage approval. | Credit score is only one factor; DTI, income, assets, and underwriting also matter. |

| DTI is the only approval requirement. | Lenders evaluate your entire financial profile. |

| Every lender uses the exact same DTI limits. | Guidelines vary by lender and loan program. |

| Paying off one credit card never helps. | Reducing monthly debt payments can improve your DTI. |

| Self-employed borrowers can’t qualify easily. | Many self-employed borrowers qualify with proper documentation. |

| FHA loans always approve high DTI borrowers. | Approval still depends on compensating factors and lender guidelines. |

Quick Summary Box

- ✔ Lower DTI generally means lower lending risk.

- ✔ Below 36% is considered an excellent target for many borrowers.

- ✔ Government-backed loans may allow higher DTI limits.

- ✔ Paying off monthly debt usually improves approval odds.

- ✔ Increasing documented income can strengthen your application.

- ✔ Avoid opening new credit accounts before closing.

- ✔ Strong credit, savings, and stable employment can offset a slightly higher DTI in some cases.

Mortgage Application Checklist: Before You Apply

Use this checklist to improve your chances of approval:

- ✅ Review your credit reports for accuracy.

- ✅ Calculate your current DTI.

- ✅ Pay down high-interest debt where possible.

- ✅ Avoid new loans and credit cards.

- ✅ Save for your down payment and closing costs.

- ✅ Build an emergency fund or cash reserves.

- ✅ Gather recent pay stubs and tax returns.

- ✅ Organize bank statements and asset documentation.

- ✅ Compare multiple mortgage lenders.

- ✅ Request a mortgage pre-approval before shopping for homes.

Conclusion

Understanding what is a good debt-to-income ratio for a mortgage is one of the smartest steps you can take before applying for a home loan. Your DTI gives lenders a snapshot of how much of your monthly income is already committed to debt payments and helps them determine whether you can comfortably afford a new mortgage. While there isn’t a single “perfect” percentage, keeping your back-end DTI below 36% generally puts you in a strong position for many loan programs. Ratios up to 43% are commonly accepted, and some FHA, VA, and USDA loans may allow higher DTIs when borrowers have strong compensating factors such as excellent credit, stable employment, or substantial cash reserves.

Remember that your DTI is only one piece of your financial profile. Mortgage lenders also evaluate your credit score, employment history, income stability, down payment, assets, and the type of loan you’re applying for. If your DTI is currently higher than you’d like, don’t assume homeownership is out of reach. Paying down debt, increasing documented income, avoiding new loans, and shopping with multiple lenders can significantly improve your chances of approval.

Most importantly, use DTI as a planning tool—not just an approval requirement. Buying a home should strengthen your financial future, not strain your monthly budget. If you’re unsure how your personal finances fit lender guidelines, speak with a licensed mortgage professional who can review your situation and recommend the loan program that best fits your goals.

Frequently Asked Questions (FAQs)

1. What is a good debt-to-income ratio for a mortgage?

For many borrowers, a DTI below 36% is considered strong. Many conventional lenders prefer ratios under 43%, while some government-backed loan programs may permit higher DTIs if the borrower has compensating strengths.

2. What DTI ratio do most mortgage lenders require?

Requirements vary by lender and loan program. Conventional loans often favor lower DTIs, while FHA, VA, and USDA loans may offer more flexibility.

3. Can I qualify for a mortgage with a 50% DTI?

Possibly. Some loan programs allow higher DTIs, but approval depends on factors such as your credit score, cash reserves, income stability, and lender guidelines.

4. What debts count toward my DTI?

Lenders typically include:

- Mortgage or rent (when applicable)

- Credit card minimum payments

- Auto loans

- Student loans

- Personal loans

- Child support

- Alimony

- HOA dues

- Property taxes

- Homeowners insurance

- Mortgage insurance

5. What expenses are not included in DTI?

Generally, lenders do not include everyday living expenses such as:

- Utilities

- Groceries

- Internet

- Cell phone bills

- Gasoline

- Entertainment

- Streaming services

6. Is front-end DTI different from back-end DTI?

Yes.

Front-end DTI measures housing expenses only.

Back-end DTI includes housing costs plus all recurring monthly debt obligations.

Most lenders place greater emphasis on the back-end ratio.

7. How do lenders calculate the debt-to-income ratio?

The formula is:

Total Monthly Debt Payments ÷ Gross Monthly Income × 100

For example:

Monthly Debt = $2,400

Monthly Income = $8,000

DTI = 30%

8. Does my credit score affect DTI?

No.

Your credit score and DTI are separate factors.

However, both significantly influence mortgage approval decisions.

9. How can I lower my DTI quickly?

Some of the fastest strategies include:

- Paying off credit card balances

- Eliminating personal loans

- Refinancing existing debt

- Increasing documented income

- Delaying major purchases before applying

10. Do student loans count toward DTI?

Yes.

Even if student loans are deferred, lenders may still include a calculated monthly payment depending on the loan program.

11. Can self-employed borrowers qualify with a higher DTI?

Yes, provided they can document stable and sufficient income. Lenders usually review tax returns, business financial statements, and other documentation to verify earnings.

12. Should I get pre-approved before house hunting?

Absolutely.

A mortgage pre-approval helps you:

- Understand your borrowing capacity

- Identify potential issues early

- Strengthen purchase offers

- Shop within a realistic budget