Mortgage Tips For Single Home Buyers: Buying your first home without a spouse can feel intimidating. You’re responsible for the down payment, monthly mortgage payment, closing costs, and every financial decision that comes with homeownership. That responsibility can seem overwhelming at first. The good news is that millions of Americans successfully purchase homes on their own every year, and lenders are increasingly familiar with working with single home buyer mortgage applications.

The biggest difference between buying alone and buying with a partner isn’t the mortgage process itself. It’s that every financial calculation depends entirely on your income, savings, credit score, and debt. That means preparation matters even more. If you understand how lenders evaluate applications, create a realistic budget, and choose the right loan program, buying a home alone is absolutely achievable.

This guide explains everything a solo home buyer needs to know—from improving mortgage approval chances to comparing lenders, selecting the right loan, avoiding expensive mistakes, and building long-term financial security.

Why Are More Americans Buying Homes Alone?

Buying a house alone is no longer unusual. Across the United States, more professionals, divorced individuals, and single parents are choosing homeownership before marriage—or instead of marriage altogether. Rising incomes, flexible careers, and remote work have made independent homeownership much more common.

Many people also realize that waiting for the “perfect time” or the “perfect partner” could delay building wealth for years. Real estate remains one of the most reliable long-term investments, and purchasing earlier often means gaining equity sooner.

Single buyers typically include:

- Young professionals

- Divorced adults

- Widows and widowers

- Single parents

- Entrepreneurs

- Military veterans

- Remote workers

Owning a home isn’t about your relationship status—it’s about financial readiness.

Advantages of Buying a Home as a Single Person

Buying a home alone comes with challenges, but it also offers benefits many people overlook.

First, every decision belongs to you. You choose the neighborhood, budget, home style, renovations, and future plans without compromise.

Second, every dollar of appreciation belongs to you. As your home’s value increases and your mortgage balance decreases, you build equity that strengthens your personal financial future.

Other advantages include:

| Benefit | Why It Matters |

|---|---|

| Full ownership | No shared legal ownership |

| Complete financial control | Easier budgeting decisions |

| Greater flexibility | Sell or refinance when needed |

| Equity growth | Build long-term wealth |

| Tax advantages | Potential homeowner deductions |

Pro Tip

Choose a monthly payment that still leaves room for vacations, retirement savings, and emergencies. Being “house rich but cash poor” can quickly create financial stress.

Challenges Single Home Buyers Should Prepare For

Qualifying on one income is the biggest obstacle for many buyers. Lenders evaluate your ability to repay the loan based on your income alone, making factors like your credit score, DTI ratio, and employment history even more important.

Unexpected home expenses can also hit harder when you’re the only person paying the bills. Roof repairs, plumbing issues, HVAC replacement, and appliance failures often arrive without warning.

That’s why experts recommend keeping an emergency fund equal to three to six months of living expenses even after closing on your home.

Another challenge is emotional. Buying a home involves dozens of decisions. Having trusted professionals—a knowledgeable real estate agent, experienced loan officer, and qualified home inspector—can make the process much less stressful.

How Much House Can You Really Afford?

Many first-time buyers focus on the maximum amount a lender will approve. That’s the wrong starting point.

Instead, ask yourself:

“How much house can I comfortably afford while still enjoying my lifestyle?”

Your housing budget should include:

- Monthly mortgage payment

- Property taxes

- Homeowners insurance

- HOA fees (if applicable)

- Utilities

- Maintenance

- Internet

- Emergency repairs

Sample Monthly Budget

| Expense | Monthly Estimate |

|---|---|

| Mortgage Payment | $1,650 |

| Property Taxes | $280 |

| Insurance | $120 |

| HOA | $90 |

| Utilities | $260 |

| Maintenance Savings | $200 |

| Total Housing Cost | $2,600 |

Many financial advisors recommend keeping total housing costs below about 28% of your gross monthly income, although every situation is different.

Understanding Credit Score

Your good credit score can dramatically improve your mortgage options.

Generally speaking:

| Credit Score | Mortgage Impact |

|---|---|

| 760+ | Excellent rates |

| 700–759 | Very competitive |

| 680–699 | Good |

| 620–679 | Acceptable for many loans |

| Below 620 | Limited options |

Improving your credit score before applying can save thousands of dollars over the life of your mortgage.

Ways to improve it include:

- Pay every bill on time.

- Keep credit utilization low.

- Avoid opening unnecessary credit accounts.

- Correct errors on your credit reports.

- Avoid large purchases before closing.

Debt-to-Income Ratio (DTI) Explained

Your debt-to-income ratio compares your monthly debt payments with your monthly gross income.

Example:

Monthly income: $6,000

Debt payments:

- Car loan: $350

- Student loan: $250

- Credit cards: $150

Total debt = $750

DTI = 12.5%

Once the new mortgage is included, lenders evaluate whether your total debt remains within acceptable guidelines.

Lower DTI generally means:

- Better approval odds

- Better interest rates

- More borrowing flexibility

Saving for a Down Payment

Contrary to popular belief, you don’t always need 20% down.

Common loan options include:

| Loan Type | Typical Down Payment |

|---|---|

| Conventional | 3%–20% |

| FHA Loan | 3.5% |

| VA Loan | 0% (eligible veterans) |

| USDA Loan | 0% (eligible rural properties) |

Even with a smaller down payment, remember to budget for closing costs, moving expenses, and initial repairs.

Building an Emergency Fund

Buying your first home should not drain every dollar from your savings account.

Aim to keep:

- 3–6 months of living expenses

- Extra cash for repairs

- Moving costs

- Furniture

- Appliance replacements

Cash reserves provide peace of mind and reduce financial stress after closing.

Choosing Between FHA, Conventional, VA, and USDA Loans

Each mortgage program serves different buyers.

| Loan | Best For | Down Payment |

|---|---|---|

| FHA Loan | Lower credit borrowers | 3.5% |

| Conventional Loan | Strong credit | 3–20% |

| VA Loan | Eligible veterans | 0% |

| USDA Loan | Rural buyers | 0% |

The best mortgage for first-time buyers depends on income, location, military eligibility, and financial goals.

Mortgage Pre-Approval Matters

Getting a mortgage preapproval before shopping gives you several advantages.

It helps you:

- Understand your realistic budget.

- Show sellers you’re serious.

- Speed up the buying process.

- Identify potential credit issues early.

During pre-approval, lenders typically review:

- Income

- Employment

- Tax returns

- Bank statements

- Credit reports

- Debt obligations

Pre-approval is different from prequalification because it involves verifying your financial information more thoroughly.

Comparing Mortgage Offers

Never accept the first offer.

Compare multiple lenders by reviewing:

- Interest rate

- APR

- Closing costs

- Origination fees

- PMI requirements

- Customer service

- Loan processing times

A slightly lower rate could save tens of thousands of dollars over the life of the loan.

Understanding Mortgage Insurance (PMI)

If your conventional loan has less than a 20% down payment, you’ll likely pay private mortgage insurance (PMI).

PMI protects the lender—not the borrower.

The good news is that PMI can often be removed once you build enough home equity.

Hidden Costs of Homeownership

Many first-time buyers underestimate ongoing expenses.

These include:

- Lawn care

- HVAC servicing

- Roof maintenance

- Pest control

- Appliance replacement

- Plumbing repairs

- HOA assessments

- Home improvements

Budgeting for these costs helps avoid financial surprises.

Home Inspection Is Never Optional

Skipping a home inspection to make your offer more attractive can become one of the most expensive mistakes you’ll ever make.

Professional inspections identify:

- Structural damage

- Electrical issues

- Plumbing problems

- Roofing concerns

- Foundation cracks

- Water damage

The inspection fee is small compared with unexpected repair costs.

Common Mistakes Single Buyers Should Avoid

Some of the biggest mistakes include:

- Buying more house than they can comfortably afford.

- Ignoring emergency savings.

- Not comparing lenders.

- Applying for new credit before closing.

- Skipping inspections.

- Forgetting about property taxes and insurance.

- Draining retirement accounts for a down payment.

Learning from others’ mistakes can save years of financial stress.

Building Home Equity

Every mortgage payment gradually increases your ownership in the property.

You can build equity faster by:

- Making extra principal payments.

- Choosing a shorter loan term.

- Improving the property.

- Buying in growing neighborhoods.

- Refinancing when appropriate.

Home equity becomes a valuable financial asset over time.

When Waiting Makes More Sense

Buying immediately isn’t always the right decision.

Consider waiting if:

- Your employment is unstable.

- Your credit score needs improvement.

- You have high-interest debt.

- You lack emergency savings.

- You’re planning to relocate soon.

Patience today can lead to better mortgage terms tomorrow.

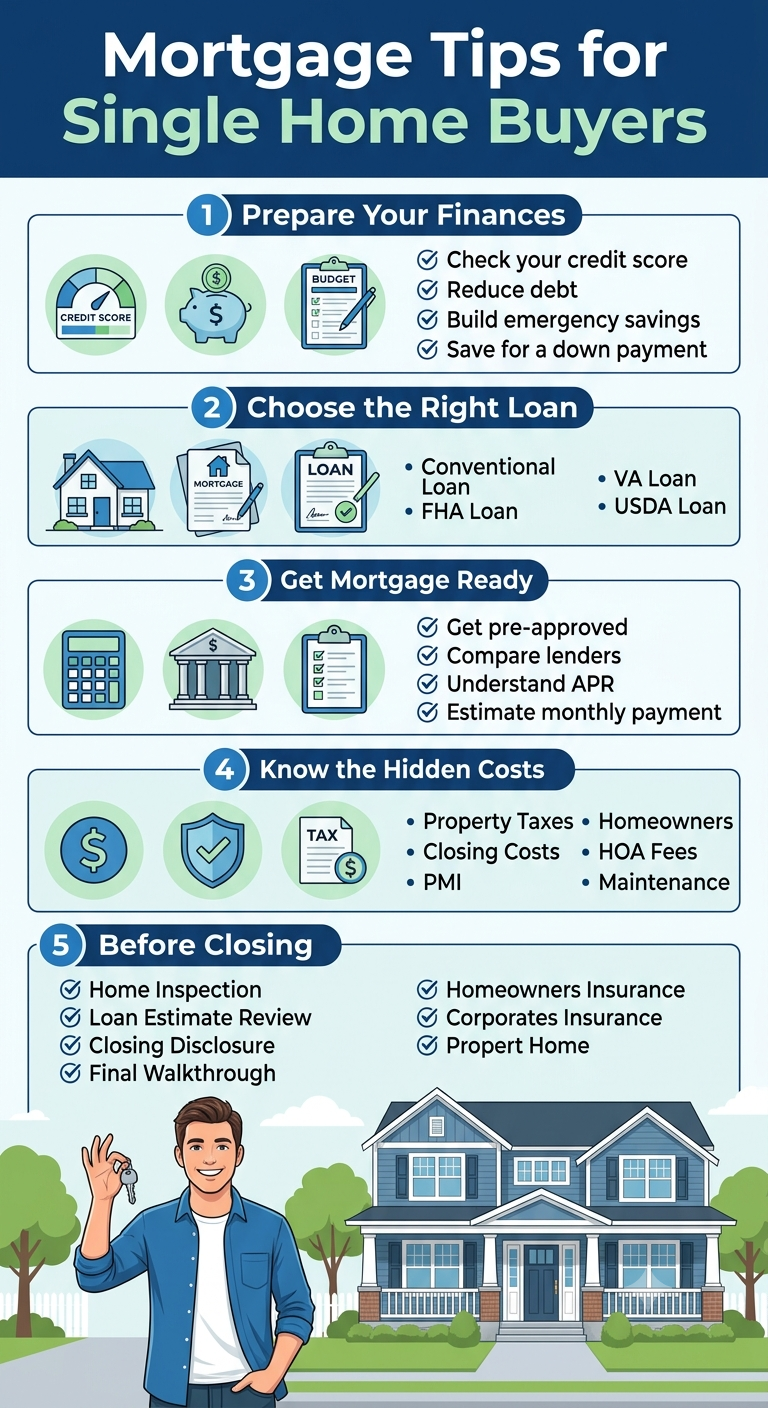

Quick Summary

Before buying a house alone:

- ✔ Check your credit score.

- ✔ Reduce debt.

- ✔ Save for a down payment.

- ✔ Build emergency savings.

- ✔ Get mortgage pre-approved.

- ✔ Compare multiple lenders.

- ✔ Understand all ownership costs.

- ✔ Never skip the home inspection.

Conclusion

Buying a home as a single person requires careful planning, but it also creates an incredible opportunity to build long-term wealth and financial independence. Focus on what you can control: strengthen your credit profile, create a realistic housing budget, compare several mortgage lenders, and understand every cost before signing. The strongest buyers aren’t necessarily those with the highest income—they’re the ones who prepare well, stay patient, and make informed decisions. With the right strategy, buying your first home alone can become one of the smartest financial moves you’ll ever make.

Frequently Asked Questions (FAQs)

1. Can I qualify for a mortgage with only one income?

Yes. Lenders regularly approve mortgages for single buyers as long as their income, credit score, debt-to-income ratio, and financial history meet their requirements.

2. What credit score is best for buying a home?

A score of 740 or higher typically qualifies borrowers for the most competitive mortgage interest rates, although many loan programs accept lower scores.

3. Is a 20% down payment required?

No. Many first-time buyers qualify with as little as 3% down on conventional loans or 3.5% on FHA loans. Eligible VA and USDA borrowers may qualify with no down payment.

4. Should I get pre-approved before looking at homes?

Absolutely. Mortgage pre-approval helps define your budget, strengthens your offer, and speeds up the home-buying process.

5. What’s the biggest mistake single home buyers make?

One of the most common mistakes is buying a house that they can comfortably afford. Leaving room in your budget for emergencies, maintenance, and future goals is just as important as qualifying for the mortgage.