What Credit Score Is Needed For A Mortgage Loan: Buying a home is one of the biggest financial decisions most Americans will ever make. Whether you’re purchasing your very first house, upgrading to a larger property, or refinancing an existing mortgage, your credit score can significantly influence your approval odds, loan options, and even how much you’ll pay over the life of your loan.

If you’ve been asking, “What Credit Score Is Needed for a Mortgage in 2026?”, you’re not alone. Mortgage lenders continue to place strong emphasis on creditworthiness, but the good news is that there isn’t a single magic number that guarantees approval. Different loan programs—including Conventional, FHA, VA, USDA, and Jumbo loans—have different credit score expectations, and many lenders also apply their own underwriting standards.

Your FICO Score remains one of the most important factors in the mortgage approval process, but lenders also review your debt-to-income ratio, employment history, down payment, available cash reserves, and overall financial profile before making a final lending decision. Even borrowers with fair or less-than-perfect credit may qualify under the right circumstances.

Why Does Your credit score matter for a Mortgage Loan?

When a lender reviews your mortgage application, they’re trying to answer one simple question: How likely are you to repay the loan on time?

Your credit score serves as a quick snapshot of your borrowing history. A higher score generally tells lenders that you’ve consistently paid bills on time, managed debt responsibly, and avoided serious financial issues. As a result, borrowers with stronger credit profiles often qualify for lower interest rates, reduced fees, and more loan choices.

A lower score doesn’t automatically prevent you from buying a home. Government-backed loan programs such as FHA Loans and many VA loans are designed to help borrowers who may not have perfect credit. Even so, improving your score before applying can potentially save tens of thousands of dollars over the life of a mortgage by reducing your interest rate. Recent analyses show that borrowers with scores above 760 often receive the best pricing, while those around 620 may pay substantially more each month for the same loan amount.

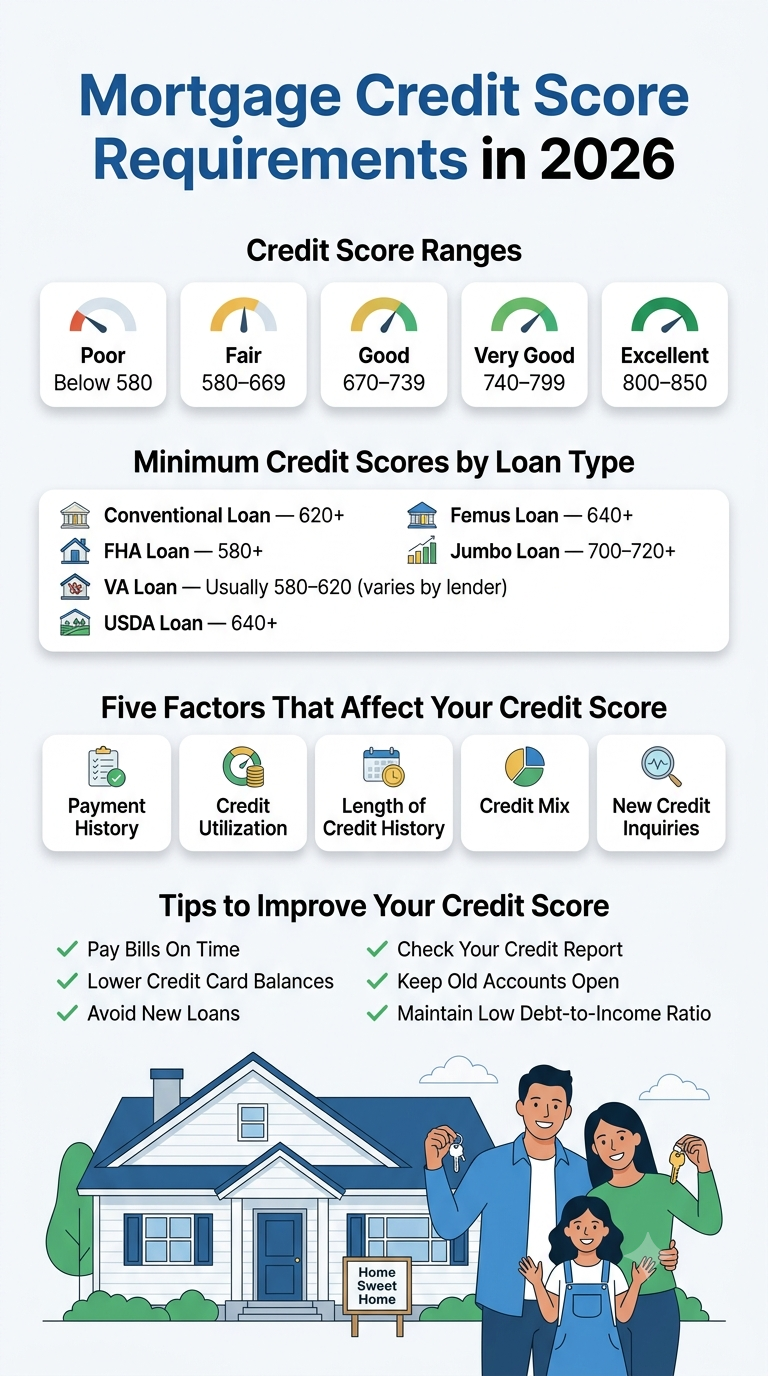

Minimum Credit Score Requirements by Loan Type

Although lender overlays vary, these are the commonly accepted minimum credit score benchmarks for major U.S. mortgage programs in 2026.

| Loan Type | Typical Minimum Credit Score | Down Payment |

|---|---|---|

| Conventional Loan | 620+ | 3% minimum |

| FHA Loan | 580 (3.5% down) / 500 (10% down) | 3.5%–10% |

| VA Loan | No official VA minimum (many lenders prefer 580–620+) | Often 0% |

| USDA Loan | Typically 640+ | 0% |

| Jumbo Loan | 700–720+ | Usually 10–20% |

These are program guidelines, not guarantees. Individual mortgage lenders frequently establish stricter internal requirements depending on market conditions, borrower risk, and loan size.

What Is Considered a Good Credit Score?

Understanding where your credit score falls is one of the easiest ways to estimate your mortgage options. While every lender has its own underwriting guidelines, most rely on FICO Score ranges when evaluating borrowers. Your score doesn’t simply determine whether you’ll qualify for a mortgage—it also affects the interest rate, loan terms, required down payment, and even whether you’ll need to pay higher mortgage insurance premiums. A borrower with a score of 780 and another with a score of 620 may both receive mortgage approvals, but the total cost of borrowing can be dramatically different over the life of the loan.

The generally accepted FICO Score ranges are shown below.

| Credit Score | Rating | Mortgage Outlook |

|---|---|---|

| Below 580 | Poor | Limited options, mainly FHA with compensating factors |

| 580–669 | Fair | FHA, VA, USDA (if eligible), some Conventional loans |

| 670–739 | Good | Strong approval chances with competitive rates |

| 740–799 | Very Good | Better pricing and lower monthly payments |

| 800–850 | Excellent | Best available mortgage offers from many lenders |

A good credit score for a mortgage generally starts around 670, while borrowers with scores above 740 often receive the most competitive mortgage rates. That doesn’t mean someone with a 620 score cannot buy a house. Many first-time buyers successfully qualify every year using FHA or Conventional loans with higher interest rates or additional compensating factors such as stable income, lower debt, or a larger down payment.

It’s also important to understand that lenders usually don’t rely on the credit score you see through a banking app or free credit monitoring service. Mortgage lenders often use specialized versions of FICO Scores generated from reports provided by Experian, Equifax, and TransUnion. These mortgage-specific scores may differ slightly from your consumer credit score, which surprises many applicants during the pre-approval process.

If you’re planning to buy a home within the next six to twelve months, now is the ideal time to review your credit reports, dispute any inaccuracies, pay down revolving debt, and avoid taking on unnecessary loans. Even a modest increase of 20 to 40 points can improve your mortgage options and potentially save thousands of dollars over the life of your loan.

Can You Get a Mortgage with Bad Credit?

One of the biggest misconceptions among home buyers is that a low credit score automatically ends their dream of homeownership. Fortunately, that isn’t true. While having bad credit certainly makes the mortgage process more challenging, several loan programs are specifically designed to help borrowers with less-than-perfect credit histories.

For example, FHA loans remain one of the most popular options for borrowers with lower credit scores. Applicants with a 580 FICO Score may qualify with as little as a 3.5% down payment, while some borrowers with scores between 500 and 579 can still qualify if they are able to make a 10% down payment. These loans are backed by the Federal Housing Administration, allowing lenders to accept borrowers who might not qualify for conventional financing.

Veterans and eligible military members have another excellent option through VA loans. The Department of Veterans Affairs does not establish an official minimum credit score requirement. Instead, individual lenders create their own standards, and many approve borrowers with scores around 580 to 620, provided the rest of the financial profile is strong.

Borrowers purchasing homes in eligible rural areas may also qualify for USDA loans, which frequently prefer credit scores of 640 or higher, although exceptions are sometimes made after manual underwriting.

Compensating Factors That Can Help

Even if your credit score is below the preferred range, lenders may consider several positive factors that reduce lending risk.

- A larger down payment

- Stable employment history

- Low debt-to-income ratio

- Significant cash reserves

- Higher household income

- Few recent late payments

- Strong rental payment history

- Low overall debt balances

These compensating factors demonstrate financial responsibility beyond the credit score itself.

Pro Tip: Never assume you’ll be denied simply because your score isn’t perfect. Many borrowers are surprised to discover they qualify after speaking with an experienced loan officer who understands multiple lending programs.

Myth vs. Fact

| Myth | Fact |

|---|---|

| You need a 700+ credit score to buy a house. | Many borrowers qualify with scores as low as 580 through FHA loans. |

| Bad credit always means mortgage denial. | Other financial strengths can offset lower credit scores. |

| Every lender has the same requirements. | Mortgage guidelines vary significantly between lenders. |

| Improving your score takes years. | Many borrowers see noticeable improvements within a few months by reducing debt and making on-time payments. |

Buying a home with fair or even poor credit isn’t impossible—it simply requires choosing the right loan program, improving your financial profile where possible, and working with a lender willing to evaluate your complete application rather than focusing solely on your credit score.

How Mortgage Lenders Actually Evaluate Your Credit Score?

Many home buyers believe that lenders simply look at a three-digit credit score and make an approval decision. In reality, that’s only a small part of the underwriting process. Mortgage lenders take a much deeper look into your financial history because they are lending hundreds of thousands of dollars over a period that could last 15 to 30 years. They want evidence that you’ll consistently make your payments, even during unexpected financial challenges.

Your mortgage approval credit score is important, but lenders also analyze your complete credit report, payment habits, debt levels, employment stability, income consistency, savings, and existing financial obligations. This is why two borrowers with identical credit scores can receive completely different mortgage offers. One applicant may have a stable job, low debt, and substantial savings, while another may have frequent late payments, high credit utilization, and limited cash reserves. Underwriters consider the entire financial picture before making a final lending decision.

The Five Major Credit Score Factors

1. Payment History (The Most Important Factor)

Your payment history makes up the largest portion of your FICO Score. Mortgage lenders want to see a consistent record of paying obligations on time because past behavior is often viewed as a strong predictor of future repayment habits.

They carefully review:

- Credit card payments

- Auto loans

- Student loans

- Personal loans

- Previous mortgages

- Collection accounts

- Bankruptcies

- Foreclosures

- Late payment history

Even one recent 30-day late payment can raise concerns, while multiple missed payments within the last year may significantly reduce your approval chances.

2. Credit Utilization

Credit utilization measures how much of your available revolving credit you’re currently using.

For example:

- Credit card limit: $10,000

- Current balance: $2,000

- Credit utilization: 20%

Most mortgage professionals recommend keeping utilization below 30%, while borrowers with utilization below 10% often have stronger credit profiles.

High balances—even if payments are made on time—can signal financial stress and reduce your credit score.

3. Length of Credit History

Lenders also value stability.

Someone who has responsibly managed credit accounts for 12 years generally appears less risky than someone whose oldest account is only one year old.

Length of credit history includes:

- Age of the oldest account

- Average age of all accounts

- How long have revolving accounts remained open

This is one reason financial experts usually recommend avoiding the unnecessary closure of older credit cards, especially if they have no annual fee.

4. Credit Mix

Mortgage lenders like to see that borrowers can responsibly manage different kinds of debt.

A healthy credit profile may include:

- Credit cards

- Auto loans

- Student loans

- Personal loans

- Installment loans

- Previous mortgage loans

Having only one type of account doesn’t automatically hurt your approval chances, but a diversified credit history often contributes positively to your overall FICO Score.

5. New Credit Inquiries

Every time you apply for new credit, the lender may perform a hard inquiry on your credit report.

Too many hard inquiries within a short period can indicate increased borrowing risk.

Examples include:

- Applying for multiple credit cards

- Financing furniture

- Taking out personal loans

- Applying for an auto loan shortly before buying a house

Fortunately, mortgage shopping works differently.

The major credit scoring models generally treat multiple mortgage inquiries completed within a designated shopping window (often 14 to 45 days, depending on the scoring model) as a single inquiry. This allows buyers to compare mortgage offers without significantly damaging their credit scores.

Important Note: Avoid opening new credit accounts after you’ve received mortgage pre-approval. Even a financed appliance or a new credit card could affect your debt-to-income ratio and potentially delay final loan approval.

Does Your Credit Score Affect Mortgage Interest Rates?

Absolutely—and often by far more than borrowers expect.

Many people focus only on qualifying for a mortgage, but the real financial impact comes from the interest rate attached to the loan. Even a small difference of half a percentage point can translate into thousands—or even tens of thousands—of dollars in additional interest over a 30-year mortgage.

Here’s why.

Mortgage lenders price loans based on risk. Borrowers with excellent credit have historically demonstrated responsible borrowing habits, making them less likely to miss payments. Because the lender assumes less risk, these borrowers are often rewarded with lower mortgage interest rates.

On the other hand, borrowers with fair or poor credit typically receive higher interest rates because lenders view them as carrying greater repayment risk.

Example: How Credit Score Can Affect Monthly Payments

The following example illustrates how different credit scores can influence borrowing costs on a $400,000 30-year fixed-rate mortgage. Actual rates vary daily and by lender, but the comparison demonstrates the long-term impact.

| Credit Score | Estimated Interest Rate | Approximate Monthly Principal & Interest |

|---|---|---|

| 800+ | Lower Available Rate | Lower Monthly Payment |

| 760–799 | Very Competitive Rate | Slightly Higher |

| 700–759 | Competitive Rate | Moderate Payment |

| 660–699 | Above Average Rate | Higher Payment |

| 620–659 | Higher Risk Pricing | Significantly Higher Payment |

Over the lifetime of a mortgage, the borrower with the stronger credit score could save tens of thousands of dollars in interest compared to someone with a lower score.

Why do Higher Scores Save More Than Just Interest?

A stronger credit profile may also help you:

- Qualify for lower closing costs

- Reduce lender fees

- Access more loan products

- Qualify with a smaller down payment

- Improve refinancing opportunities later

- Increase negotiating power with lenders

For first-time home buyers especially, improving a credit score before applying for a mortgage often provides one of the highest financial returns possible. Waiting a few extra months to raise your score could result in lower monthly payments for decades.

Pro Tip: Request mortgage quotes from several lenders within a short shopping period. Comparing multiple Loan Estimates allows you to find the best combination of interest rate, fees, and closing costs without causing significant additional impact to your credit score.

How to Improve Your Credit Score Before Applying for a Mortgage Loan?

If you’re planning to buy a home within the next few months, improving your credit score can be one of the smartest financial moves you make. While no strategy can guarantee a specific score increase, many borrowers see meaningful improvements by adopting healthy credit habits and correcting issues that may be dragging down their profile. Even a modest increase of 20 to 40 points could help you qualify for a better interest rate, a lower monthly payment, or more favorable loan terms.

The first step is to obtain copies of your credit reports from Experian, Equifax, and TransUnion. Review each report carefully for inaccurate late payments, duplicate accounts, incorrect balances, or accounts that don’t belong to you. Credit reporting errors are more common than many people realize, and disputing inaccurate information can sometimes result in a noticeable score improvement. At the same time, continue making every payment on or before its due date. Payment history carries the greatest weight in most credit scoring models, so a consistent record of on-time payments is one of the most effective ways to build stronger credit.

Another powerful strategy is reducing your credit utilization ratio. If your credit cards are close to their limits, paying down balances can quickly improve your score. Many financial experts recommend keeping utilization below 30%, while staying under 10% is often even more beneficial. Avoid closing old credit card accounts unless there’s a compelling reason, as longer credit histories generally strengthen your credit profile. If you’re preparing for a mortgage application, it’s also wise to postpone opening new credit cards, financing furniture, or taking out personal loans, since these actions can increase your debt and generate additional hard inquiries.

Practical Steps That Often Produce Results

The following checklist summarizes some of the most effective ways to improve your mortgage credit profile before applying.

✔ Pay every bill on time, without exception.

✔ Reduce revolving credit card balances.

✔ Keep credit utilization below 30%, ideally below 10%.

✔ Review all three credit reports for errors.

✔ Dispute inaccurate information promptly.

✔ Avoid applying for unnecessary new credit.

✔ Maintain steady employment and income.

✔ Build an emergency savings fund.

✔ Continue making payments on existing loans.

✔ Avoid large purchases before closing on your mortgage.

Warning Box

Warning: Many home buyers make major purchases immediately after receiving mortgage pre-approval, such as financing furniture, appliances, or a new vehicle. This can increase your debt-to-income ratio and may even jeopardize your final mortgage approval. Wait until after your home purchase has officially closed before taking on additional debt.

Improving your credit score isn’t about finding shortcuts or “credit hacks.” Instead, it’s about demonstrating consistent financial responsibility over time. Mortgage lenders appreciate stability, and the healthier your overall financial profile becomes, the stronger your application will be.

Common Credit Score Mistakes Home Buyers Make

Buying a home is exciting, but it’s also easy to make mistakes that unintentionally weaken your mortgage application. Many borrowers focus solely on reaching the minimum credit score requirement while overlooking other financial behaviors that lenders carefully evaluate. Avoiding these common pitfalls can improve your chances of approval and help you secure a more competitive mortgage.

One of the biggest mistakes is assuming that checking your own credit score will hurt it. Fortunately, reviewing your personal credit reports through authorized services typically results in a soft inquiry, which has no impact on your score. In contrast, applying for several new credit cards or personal loans before your mortgage application creates hard inquiries, which can temporarily lower your score and raise concerns for lenders.

Another frequent mistake is carrying high credit card balances despite making minimum payments on time. While paying on time is essential, high utilization ratios can still negatively affect your credit score. Similarly, some borrowers believe closing unused credit cards will improve their credit profile, but closing long-standing accounts can reduce available credit and shorten the average age of accounts, both of which may lower your score.

Many first-time buyers also underestimate the importance of maintaining stable employment. Although changing jobs doesn’t automatically disqualify you from obtaining a mortgage, frequent employment changes or interruptions in income may require additional documentation during underwriting. Keeping detailed financial records, avoiding unnecessary debt, and maintaining steady employment all contribute to a stronger mortgage application.

Myth vs. Fact

| Myth | Fact |

|---|---|

| Paying off a credit card and immediately closing it always improves your score. | Closing older accounts can sometimes reduce your score by affecting credit history and available credit. |

| You should avoid comparing mortgage lenders because every inquiry hurts your credit. | Mortgage inquiries made within a designated shopping window are generally treated as a single inquiry by many FICO scoring models. |

| A high income guarantees mortgage approval. | Income is important, but lenders also evaluate credit history, debt-to-income ratio, assets, and overall financial stability. |

| Once you’re pre-approved, your finances no longer matter. | Lenders continue reviewing your financial profile until closing, so avoid new debt and late payments throughout the process. |

Pro Tips for Mortgage Applicants

- Start preparing your credit profile at least six months before buying a home.

- Save more than the minimum required down payment if possible.

- Keep detailed documentation of your income and assets.

- Compare Loan Estimates from multiple lenders before making a decision.

- Ask your loan officer about programs for first-time buyers, veterans, or rural borrowers if you qualify.

- Remember that mortgage requirements vary by lender, loan program, and current market conditions.

By avoiding these common mistakes and following sound financial habits, you’ll place yourself in a much stronger position when it’s time to apply for a mortgage. Even if your credit score isn’t perfect today, thoughtful preparation can make a significant difference in both your approval chances and the total cost of your home loan.

Conclusion

Buying a home in 2026 is about far more than simply reaching a specific credit score. While many borrowers search for a single answer to “What Credit Score Is Needed for a Mortgage in 2026?”, the reality is that mortgage approval depends on your overall financial profile. Your credit score is one of the most influential factors, but lenders also examine your income, debt-to-income ratio, employment history, assets, down payment, cash reserves, and recent credit activity before making a lending decision.

As a general guideline, a 620 FICO Score is commonly considered the starting point for many Conventional loans, while FHA loans may be available to qualified borrowers with scores as low as 580, and in certain situations, even 500 with a larger down payment. VA and USDA loans offer excellent opportunities for eligible borrowers, although participating lenders often establish their own minimum credit score requirements. Borrowers with scores above 740 typically receive the most competitive mortgage rates, which can translate into substantial savings throughout the life of a home loan.

If your credit score isn’t where you’d like it to be, don’t assume homeownership is out of reach. Paying bills on time, lowering credit card balances, avoiding unnecessary debt, reviewing your credit reports for errors, and maintaining stable employment can gradually strengthen your financial profile. Even a relatively small improvement in your score could lead to better loan terms and lower monthly payments.

Mortgage lending guidelines continue to evolve as market conditions change, and every lender evaluates risk differently. Before making any major financial decisions, speak with a qualified loan officer, compare Loan Estimates from multiple lenders, and confirm the latest program requirements that apply to your specific situation. Careful preparation today can make your journey toward homeownership smoother, more affordable, and far less stressful.

Frequently Asked Questions (FAQs)

1. What credit score is needed for a mortgage Loan in 2026?

Most Conventional loans typically require a minimum credit score of around 620, while FHA loans may accept qualified borrowers with scores as low as 580. VA and USDA loans have flexible guidelines, although participating lenders often establish their own minimum score requirements.

2. Can I get a mortgage with a 620 credit score?

Yes. A 620 credit score is commonly sufficient for many Conventional mortgage programs, provided you also meet income, debt-to-income ratio, employment, and down payment requirements.

3. Can I buy a house with bad credit?

Yes. Borrowers with lower credit scores may qualify for FHA loans or other specialized lending programs. Larger down payments, lower debt, stable income, and strong financial reserves may improve approval chances.

4. What is considered a good credit score for a mortgage Loan?

A good credit score generally starts around 670, while scores of 740 or higher often qualify borrowers for the most competitive mortgage interest rates.

5. Does a higher credit score lower mortgage interest rates?

In many cases, yes. Higher credit scores often qualify for lower interest rates, reducing monthly payments and potentially saving thousands of dollars over the life of the loan.

6. Which credit score do mortgage lenders use?

Mortgage lenders commonly use specialized FICO® Score models generated from reports provided by Experian, Equifax, and TransUnion, rather than the educational scores displayed by many consumer apps.

7. How can I improve my credit score before applying?

Focus on paying bills on time, reducing credit card balances, avoiding new debt, correcting credit report errors, and maintaining low credit utilization.

8. Does checking my own credit score hurt it?

No. Checking your own credit report typically results in a soft inquiry, which does not affect your credit score.

9. Can self-employed borrowers qualify for a mortgage?

Absolutely. Self-employed applicants can qualify by providing documentation that demonstrates stable income, tax returns, and the ability to repay the loan.

10. How much does my down payment affect mortgage approval?

A larger down payment reduces lender risk, may improve approval chances, and can sometimes help borrowers with lower credit scores qualify for financing.

11. Should I pay off all my debt before applying?

Not necessarily. Instead of eliminating every debt, focus on maintaining a manageable debt-to-income ratio, paying bills consistently, and avoiding new borrowing.

12. Is mortgage pre-approval worth getting?

Yes. Mortgage pre-approval helps you understand your budget, strengthens your position when making offers, and identifies potential credit issues before beginning your home search.