Compare the best mortgage lenders for first-time home buyers in 2026. Learn how to evaluate rates, fees, and loan programs and choose the right lender with confidence.

Buying your first home is one of the biggest financial decisions you’ll ever make. While many buyers spend months comparing neighborhoods, school districts, and home prices, they often overlook something equally important—the mortgage lender. The lender you choose can affect your monthly payment, closing costs, customer experience, approval timeline, and even whether your offer reaches the closing table on time.

If you’ve been searching for the Best Mortgage Lenders for First-Time Home Buyers, you’ve probably noticed that every lender claims to be the best. The reality is much more nuanced. A lender that’s an excellent fit for a veteran using a VA loan may not be the right choice for someone purchasing a starter home with an FHA loan. Likewise, a borrower with a high credit score may qualify for different loan terms than someone who is just beginning to build credit.

Mortgage rates have remained relatively elevated during 2026, with the average 30-year fixed mortgage hovering around the mid-6% range in recent weeks, making lender comparison even more important. Even a small difference in interest rate or lender fees can translate into thousands of dollars over the life of your loan.

This guide focuses on helping you compare lenders based on real lending features rather than marketing promises. Mortgage rates, eligibility requirements, fees, and available loan programs change frequently, so always verify current information directly with each lender before making a final decision.

How to Choose the Right Mortgage Lender?

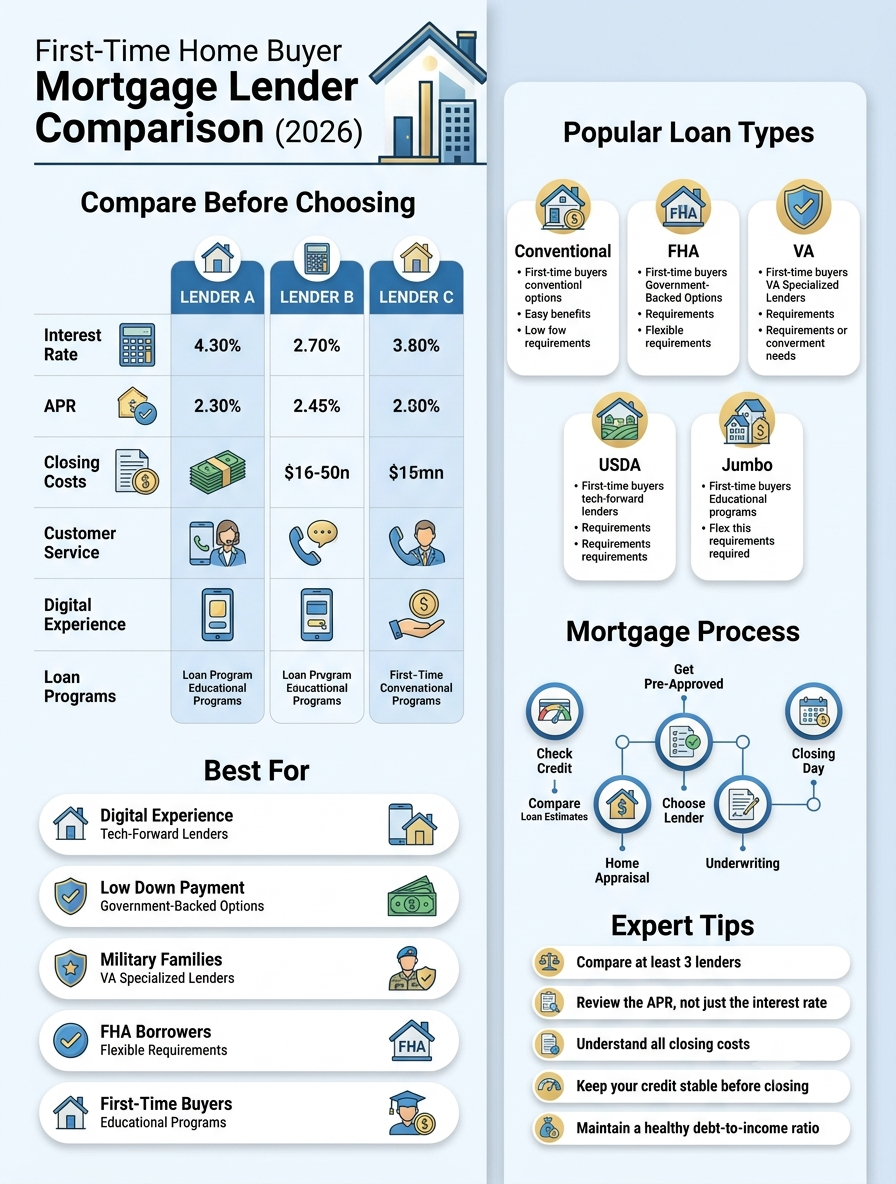

Choosing a mortgage lender isn’t simply about finding the lowest advertised interest rate. Experienced homebuyers understand that the total borrowing experience includes customer service, loan flexibility, underwriting efficiency, digital tools, closing costs, and communication throughout the process.

The Consumer Financial Protection Bureau (CFPB) recommends requesting Loan Estimates from multiple lenders before making your decision. Comparing these standardized forms side by side allows you to evaluate costs fairly and even negotiate better terms.

When evaluating lenders, pay close attention to:

- Interest Rate

- APR (Annual Percentage Rate)

- Origination Fees

- Closing Costs

- Rate Lock Options

- Loan Programs Available

- Digital Application Experience

- Customer Support

- Average Closing Time

- Loan Officer Responsiveness

One common mistake among first-time home buyers is focusing only on the advertised interest rate. Two lenders may offer the same rate, yet one may charge significantly higher origination fees or discount points. Looking at the APR gives you a more complete picture because it incorporates both the interest rate and many of the associated loan costs.

Another factor worth considering is technology. Some buyers appreciate completing nearly every step online, while others prefer speaking with a dedicated loan officer throughout the process. There is no universally “better” option—it depends on your comfort level and borrowing needs.

Interest Rate vs. APR

Many first-time buyers confuse the mortgage interest rate with the APR.

| Feature | Interest Rate | APR |

|---|---|---|

| Monthly payment | ✔ | ✔ |

| Includes lender fees | ✘ | ✔ |

| Helps compare lenders | Limited | Better |

| Reflects total borrowing cost | No | Yes |

A lender advertising the lowest rate may still end up costing more if it charges higher fees. This is why financial experts recommend comparing APRs on Loan Estimates issued around the same time.

Why Mortgage Pre-Approval Matters?

Before shopping seriously for a home, obtaining a mortgage pre-approval can strengthen your offer and clarify your budget. A pre-approval is different from a prequalification because the lender reviews your financial information, including income, assets, credit history, and debt obligations.

Benefits include:

- Stronger purchase offers

- Faster closing process

- Better understanding of affordability

- Fewer surprises during underwriting

- Ability to identify potential credit issues early

According to CFPB guidance, borrowers should request Loan Estimates from multiple lenders after identifying a property, since comparing offers can help reduce borrowing costs.

Best Mortgage Lenders for First-Time Home Buyers

Rocket Mortgage

Overview

Rocket Mortgage remains one of America’s largest online mortgage lenders and is particularly popular among buyers who prefer completing most of the mortgage process digitally. Its application platform is streamlined, making document uploads and loan tracking relatively straightforward.

Best For

- Tech-savvy borrowers

- Fast online applications

- Digital mortgage experience

- Conventional and FHA borrowers

Loan Programs

- Conventional Loans

- FHA Loans

- VA Loans

- Jumbo Loans

- Refinance Options

Online Experience

Excellent. Borrowers can upload documents, monitor progress, communicate securely, and receive updates through both desktop and mobile applications.

Customer Support

Phone, online chat, and secure messaging.

Potential Drawbacks

- It may not always offer the lowest rates available.

- Borrowers seeking extensive face-to-face assistance may prefer local lenders.

Better Mortgage

Overview

Better Mortgage has built its reputation around a fully digital mortgage process with no lender commissions. The platform provides quick online rate estimates and an intuitive application experience.

Best For

- Online borrowers

- Buyers comfortable with technology

- Fast pre-approvals

Loan Programs

- Conventional

- FHA

- VA

- Jumbo

Strengths

- User-friendly online dashboard

- Transparent digital process

- Fast document verification

Potential Drawbacks

- Limited physical branch locations.

- Some borrowers may prefer more personalized guidance.

Pennymac

Overview

Pennymac has become a well-known national mortgage lender offering a wide range of purchase and refinance products. It serves borrowers with varying financial profiles, making it attractive for many first-time buyers.

Best For

- Conventional borrowers

- FHA applicants

- Buyers comparing multiple loan options

Loan Types

- Conventional

- FHA

- VA

- USDA

- Jumbo

Strengths

- Broad loan selection

- Online account management

- Educational resources

Potential Drawbacks

- Customer experiences can vary depending on loan complexity.

Guild Mortgage

Overview

Guild Mortgage combines digital convenience with personalized loan officer support. This hybrid approach appeals to first-time buyers who appreciate technology but also want guidance throughout the buying process.

Best For

- Buyers wanting personal assistance

- Down payment assistance program seekers

- FHA borrowers

Strengths

- Strong educational resources

- Local loan officers

- Flexible loan options

Potential Drawbacks

- Availability of certain programs varies by state.

Veterans United Home Loans

Overview

Veterans United Home Loans has built a strong reputation by focusing primarily on military service members, veterans, and eligible surviving spouses. Instead of trying to serve every borrower type equally, the company specializes in VA loans, making it an excellent option for qualified first-time buyers who want expert guidance through the VA home loan process.

One reason many eligible borrowers choose Veterans United is its educational approach. Buying a first home can feel overwhelming, especially when navigating Certificate of Eligibility (COE) requirements, funding fees, and VA appraisal rules. Veterans United provides dedicated loan specialists who understand these requirements and can explain them in plain language. Rather than pushing borrowers toward a particular product, the lender focuses on matching applicants with loan programs they actually qualify for.

Best For

- Eligible veterans

- Active-duty military members

- National Guard and Reserve members

- Eligible surviving spouses

- First-time VA borrowers

Available Loan Types

- VA Purchase Loans

- VA Interest Rate Reduction Refinance Loans (IRRRL)

- VA Cash-Out Refinance

- Conventional Loans

Online Application Experience

The digital application allows borrowers to upload documentation securely, track milestones, and communicate with loan specialists. Those who prefer personal guidance can also complete much of the process over the phone.

Customer Support

One of the lender’s strongest features is its specialized customer service team dedicated to VA lending.

Potential Drawbacks

- Not the best choice for borrowers who do not qualify for VA benefits.

- FHA and USDA options are more limited compared to those of some competitors.

Navy Federal Credit Union

Overview

Navy Federal Credit Union serves military members, veterans, Department of Defense employees, and eligible family members. Because it is a credit union, it often emphasizes member service over aggressive marketing.

Many first-time buyers appreciate Navy Federal’s educational resources and flexible mortgage programs. Depending on borrower qualifications and membership eligibility, the lender offers several options designed to reduce upfront costs.

Best For

- Military families

- Credit union members

- Buyers seeking personalized service

Loan Programs

- Conventional

- VA

- FHA

- Jumbo

- Homebuyers Choice (availability varies)

Customer Experience

Navy Federal combines online tools with local branch support. Borrowers who prefer speaking directly with a mortgage specialist may appreciate this hybrid approach.

Strengths

- Strong reputation for customer satisfaction

- Multiple mortgage products

- Educational resources for first-time buyers

Potential Drawbacks

- Membership eligibility requirements apply.

- Not available to every borrower.

U.S. Bank

Overview

U.S. Bank offers one of the broadest selections of mortgage products among traditional banks. First-time buyers who already bank with U.S. Bank may appreciate having checking accounts, savings accounts, and mortgage services under one institution.

The lender provides digital mortgage tools while maintaining an extensive branch network for buyers who prefer face-to-face assistance.

Best For

- Existing U.S. Bank customers

- Buyers seeking local branch access

- Conventional borrowers

Loan Programs

- Conventional

- FHA

- VA

- USDA

- Jumbo

Strengths

- Large national presence

- Branch locations

- Multiple loan choices

- Digital mortgage platform

Potential Drawbacks

- Processing times may vary depending on loan complexity.

- Some online-only competitors provide a faster digital experience.

Chase Home Lending

Overview

Chase Home Lending remains one of the largest mortgage providers in the United States. It combines a nationwide branch network with online mortgage tools, making it attractive to borrowers who want flexibility.

Existing Chase customers may benefit from keeping their banking and mortgage relationship in one place, although every borrower should still compare Loan Estimates from multiple lenders before deciding. The CFPB recommends comparing standardized Loan Estimates because shopping around can save borrowers hundreds or even thousands of dollars over the life of a mortgage.

Best For

- Existing Chase banking customers

- Buyers wanting branch support

- Conventional financing

Loan Programs

- Conventional

- FHA

- VA

- Jumbo

Strengths

- Large branch network

- Mobile banking integration

- Educational mortgage resources

Potential Drawbacks

- Availability of certain programs depends on location.

- Not always the most competitive lender for every borrower profile.

| Lender | FHA | VA | USDA | Conventional | Jumbo | Online Application | Branch Support | Best For |

|---|---|---|---|---|---|---|---|---|

| Rocket Mortgage | ✔ | ✔ | Limited | ✔ | ✔ | Excellent | No | Digital borrowers |

| Better Mortgage | ✔ | ✔ | Limited | ✔ | ✔ | Excellent | No | Fast online approvals |

| Pennymac | ✔ | ✔ | ✔ | ✔ | ✔ | Very Good | Limited | Wide loan selection |

| Guild Mortgage | ✔ | ✔ | ✔ | ✔ | Limited | Good | Yes | Personalized service |

| Veterans United | Limited | ✔ | No | ✔ | No | Excellent | Limited | Veterans |

| Navy Federal | ✔ | ✔ | Limited | ✔ | ✔ | Very Good | Yes | Military families |

| U.S. Bank | ✔ | ✔ | ✔ | ✔ | ✔ | Very Good | Yes | Traditional banking |

| Chase Home Lending | ✔ | ✔ | Limited | ✔ | ✔ | Very Good | Yes | Existing Chase customers |

Important: Mortgage rates, lender fees, down payment requirements, and loan availability change frequently. Always request updated Loan Estimates from each lender you’re considering before making a final decision.

Best Mortgage Lenders by Borrower Type

Choosing the “best” lender depends far more on your financial situation than on brand recognition.

| Borrower Type | Suggested Lender |

|---|---|

| Low Credit Score | Guild Mortgage |

| FHA Loans | Pennymac |

| VA Loans | Veterans United |

| USDA Loans | Pennymac |

| Best Digital Experience | Rocket Mortgage |

| Fast Online Approval | Better Mortgage |

| Military Families | Navy Federal Credit Union |

| Existing Bank Customers | Chase or U.S. Bank |

Expert Tip

Don’t stop after receiving one pre-approval. Multiple mortgage inquiries completed within a short shopping window are generally treated as a single inquiry by credit scoring models, allowing you to compare lenders without the same impact as widely separated applications. Community discussions from recent first-time buyers also consistently recommend obtaining quotes from several lenders before deciding.

Questions to Ask Before Choosing a Mortgage Lender

Choosing a mortgage lender is about far more than accepting the first attractive rate you see online. A lender may advertise a competitive interest rate but charge higher origination fees, impose stricter underwriting standards, or provide less responsive customer service. Before signing any paperwork, schedule a conversation with each lender or loan officer and ask detailed questions. Their willingness to answer clearly can tell you just as much as the numbers on the Loan Estimate.

Here are some of the most important questions to ask:

- What loan programs do I qualify for?

- What is the interest rate and the APR?

- How long can you lock my interest rate?

- What are the estimated closing costs?

- Are there any lender credits or discount points available?

- How long does your average closing take?

- Will I work with one loan officer throughout the process?

- Can I complete everything online if I choose to?

- Will my loan be serviced by your company or transferred after closing?

- What happens if my closing date is delayed?

The Consumer Financial Protection Bureau (CFPB) also recommends comparing Loan Estimates from multiple lenders and using them as a negotiation tool. In many cases, lenders are willing to match or improve competing offers when presented with comparable Loan Estimates.

Common First-Time Home Buyer Mistakes

Buying your first home is exciting, but excitement sometimes leads to expensive mistakes. Fortunately, most of these errors are preventable with proper planning.

1. Shopping for a House Before Getting Pre-Approved

Many buyers start touring homes before understanding how much they can comfortably borrow. A mortgage pre-approval gives you a realistic price range and strengthens your offer when competing against other buyers.

2. Comparing Only Interest Rates

A lower interest rate doesn’t automatically mean a better mortgage. Two lenders may advertise the same rate while charging very different fees. Compare the APR, origination charges, and the five-year cost shown on your Loan Estimate rather than focusing only on the headline rate.

3. Ignoring Closing Costs

Closing costs often range from 2% to 5% of the home’s purchase price, depending on the loan and location. Buyers who budget only for the down payment may face an unexpected financial burden at closing.

4. Making Large Purchases Before Closing

Financing a new car, opening new credit cards, or taking on additional debt before closing can change your debt-to-income ratio and potentially affect your mortgage approval.

5. Failing to Compare Multiple Lenders

Many buyers accept the first mortgage offer they receive. Shopping around can lead to meaningful savings over the life of the loan. According to the CFPB, requesting multiple Loan Estimates can help borrowers save money and secure a loan that better fits their needs.

Tips to Increase Your Mortgage Approval Chances

Although no lender can guarantee approval, several practical steps can significantly strengthen your mortgage application.

Improve Your Credit Score

A higher FICO® Score generally opens the door to better mortgage terms. Even a modest improvement before applying may reduce your long-term borrowing costs. Recent mortgage market analyses continue to show that borrowers with stronger credit typically qualify for lower rates than those with fair credit.

Reduce Your Debt-to-Income Ratio

Paying down high-interest debt before applying can improve your financial profile and increase lender confidence.

Save for a Larger Down Payment

While many first-time buyer programs allow low down payments, contributing more upfront may reduce monthly payments and lower private mortgage insurance (PMI) costs.

Organize Your Financial Documents

Prepare documents such as:

- Recent pay stubs

- W-2s or tax returns

- Bank statements

- Employment verification

- Identification

- Asset documentation

Having these ready can help your application move more smoothly through underwriting.

Avoid Changing Jobs During the Process

Stable employment often makes underwriting simpler. If a career change is unavoidable, discuss it with your loan officer before making the transition.

Myth vs. Fact

| Myth | Fact |

|---|---|

| You need a 20% down payment to buy a home. | Many conventional, FHA, and VA programs allow qualified borrowers to purchase with much lower down payments. |

| The lowest advertised rate is always the best deal. | Fees, APR, discount points, and closing costs all affect the total cost of borrowing. |

| Pre-qualification and pre-approval are the same. | A pre-approval generally involves a more detailed financial review and carries more weight with sellers. |

| You should only apply with one lender. | Comparing multiple Loan Estimates is encouraged by the CFPB and can help you negotiate better terms. |

Real-Life Scenario

Imagine two first-time buyers purchasing similar $350,000 homes.

- Buyer A accepts the first lender’s offer after seeing an attractive interest rate online.

- Buyer B obtains Loan Estimates from four lenders, compares APRs, origination charges, estimated closing costs, and customer service, then negotiates with their preferred lender using a competing estimate.

Although both buyers receive similar interest rates, Buyer B ultimately pays lower upfront fees and secures a more favorable overall borrowing package. This illustrates why experienced mortgage professionals recommend evaluating the complete Loan Estimate—not just the advertised rate.

First-Time Home Buyer Checklist

Before choosing a mortgage lender, make sure you have completed the following:

- ✅ Check your credit reports.

- ✅ Estimate a comfortable monthly payment.

- ✅ Save for your down payment and closing costs.

- ✅ Compare at least three Loan Estimates.

- ✅ Review the APR—not just the interest rate.

- ✅ Understand PMI requirements.

- ✅ Ask about rate-lock options.

- ✅ Verify estimated closing timelines.

- ✅ Read customer reviews alongside official loan disclosures.

- ✅ Keep your finances stable until closing.

Key Takeaways

Choosing the right mortgage lender isn’t about finding a universally “best” company. Instead, it’s about identifying the lender whose loan programs, fees, customer support, and application process best match your financial situation and homeownership goals.

Mortgage rates, closing costs, underwriting guidelines, and available loan products change frequently. Before making a commitment, compare standardized Loan Estimates from several lenders issued around the same time, ask questions about anything you don’t understand, and evaluate both the cost and the quality of service.

With mortgage rates continuing to fluctuate around the mid-6% range in 2026, careful comparison shopping remains one of the most effective ways first-time buyers can reduce borrowing costs over the life of a loan.

Conclusion

Buying your first home is a major milestone, and choosing the right mortgage lender plays a critical role in how smooth and affordable that journey becomes. While it is tempting to focus only on the lowest advertised interest rate, experienced borrowers know that the complete mortgage package matters just as much. Loan programs, lender fees, customer service, digital tools, underwriting efficiency, and closing timelines can all influence your overall experience and long-term costs.

There is no single lender that is the best fit for every borrower. A military family using a VA loan may find that Veterans United Home Loans or Navy Federal Credit Union better suits their needs, while a buyer who prefers a fully digital application may lean toward Rocket Mortgage or Better Mortgage. Borrowers looking for a broad selection of government-backed loans might consider lenders such as Pennymac, Guild Mortgage, or U.S. Bank. The key is to match the lender’s strengths with your financial profile and homeownership goals.

Remember that mortgage rates, APRs, fees, eligibility requirements, and available loan programs change over time. Before making a final decision, request Loan Estimates from several lenders issued within the same time frame. Comparing these standardized estimates side by side can help you identify meaningful differences in total borrowing costs and make a more informed decision. This comparison process is recommended by the Consumer Financial Protection Bureau (CFPB). (consumerfinance.gov)

With careful research, realistic budgeting, and thoughtful lender comparison, you’ll be better prepared to secure financing that supports both your first home purchase and your long-term financial well-being.

Frequently Asked Questions (FAQs)

1. Which mortgage lender is best for first-time home buyers?

There isn’t a single “best” lender for everyone. The right lender depends on your credit score, down payment, loan type, customer service preferences, and financial goals. Comparing Loan Estimates from multiple lenders is the best way to identify the most suitable option.

2. How many mortgage lenders should I compare?

Financial experts generally recommend comparing at least three to five lenders. This allows you to evaluate differences in interest rates, APRs, lender fees, and customer service.

3. What credit score do I need to buy my first home?

The required credit score varies depending on the loan program and lender. Conventional loans often require higher credit scores than FHA loans, while VA and USDA loans have their own qualification standards.

4. Is mortgage pre-approval necessary?

Although not legally required, mortgage pre-approval is strongly recommended. It helps establish your budget, strengthens purchase offers, and demonstrates to sellers that you’re a serious buyer.

5. What is the difference between an interest rate and an APR?

The interest rate determines the cost of borrowing money, while the APR (Annual Percentage Rate) includes both the interest rate and many lender fees, providing a more complete estimate of the loan’s overall cost.

6. Can I get a mortgage with a low down payment?

Yes. Many loan programs allow qualified borrowers to purchase a home with a relatively small down payment. FHA, VA, USDA, and certain conventional loan programs all offer low down payment options for eligible buyers.

7. Should I choose an online mortgage lender or a local lender?

Both options have advantages. Online lenders often provide faster digital applications and convenient document management, while local lenders may offer more personalized guidance and face-to-face support.

8. How long does mortgage approval usually take?

Approval timelines vary depending on the lender, loan type, documentation, and underwriting complexity. Some digital lenders may move faster, while more complex loans can require additional time.

9. What are closing costs?

Closing costs include expenses such as lender fees, appraisal fees, title insurance, government recording fees, and other charges associated with finalizing your mortgage.

10. Can I negotiate mortgage fees?

Yes. Certain lender fees may be negotiable. Comparing Loan Estimates from multiple lenders provides leverage when discussing pricing and lender credits.

11. What documents are usually required for mortgage approval?

Most lenders request:

- Government-issued identification

- Recent pay stubs

- W-2 forms or tax returns

- Bank statements

- Employment verification

- Information about debts and assets

Additional documentation may be required depending on your financial situation.

12. How often do mortgage rates change?

Mortgage rates can change daily based on economic conditions, inflation, bond market activity, and other financial factors. Always request updated rate quotes directly from lenders before making a decision.

13. What is Private Mortgage Insurance (PMI)?

PMI is insurance that may be required on certain conventional loans when the borrower makes a down payment below the lender’s required threshold. It protects the lender rather than the borrower.

14. Should I refinance my mortgage later?

Refinancing may be beneficial if interest rates decline, your credit profile improves, or your financial goals change. Whether refinancing makes sense depends on your individual circumstances, closing costs, and expected time in the home.